Modality Agnostic

The modalities and technologies driving growth.

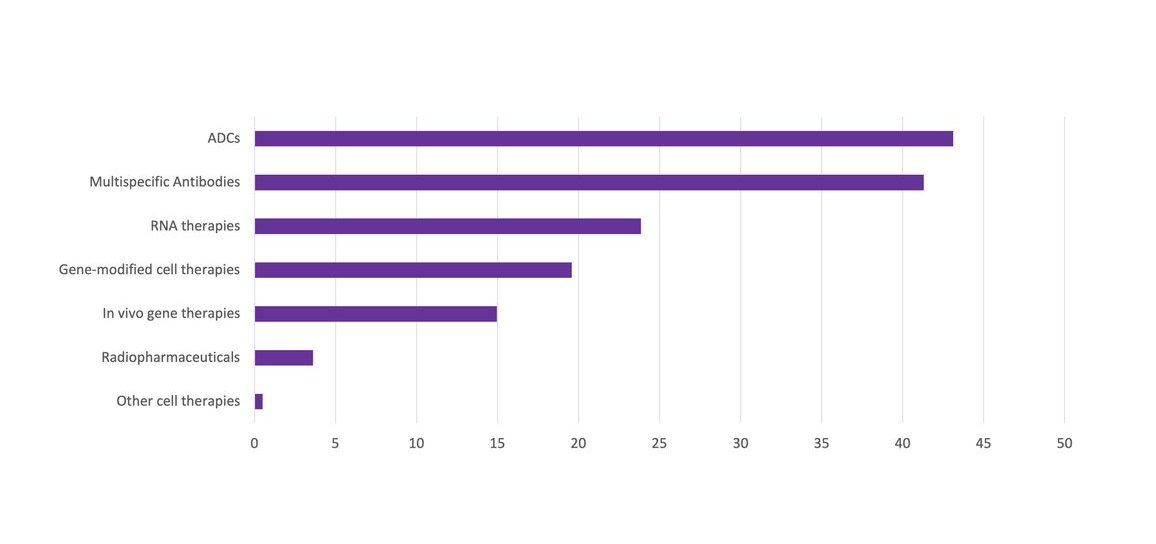

Multi-specific antibodies and antibody-drug conjugates remain popular contenders in the race for more effective cancer therapies. They lead the pack among next-generation modalities in projected 2030 sales; each will sell over $40 billion more in 2030 than in 2024.

Despite frenzied dealmaking activity around ADCs and bispecifics, many Big Pharma business development teams now describe themselves as ‘modality-agnostic’. With ever-more biology-tweaking tools in the toolbox, drug developers (and investors) are selecting whatever instrument is best for the job. “We have disease area strongholds but are modality agnostic” and will use whatever most effectively modulates the chosen target, said J&J’s Head of Innovation, East North America in 2024.

Over two thirds of the top 100 best sellers in 2030 will be biologics.

Novelty per se is far from a guarantee of commercial success. Cell- and gene-therapy companies have suffered more than most as high prices and complex, lengthy manufacturing and administration processes limit product uptake and revenues.

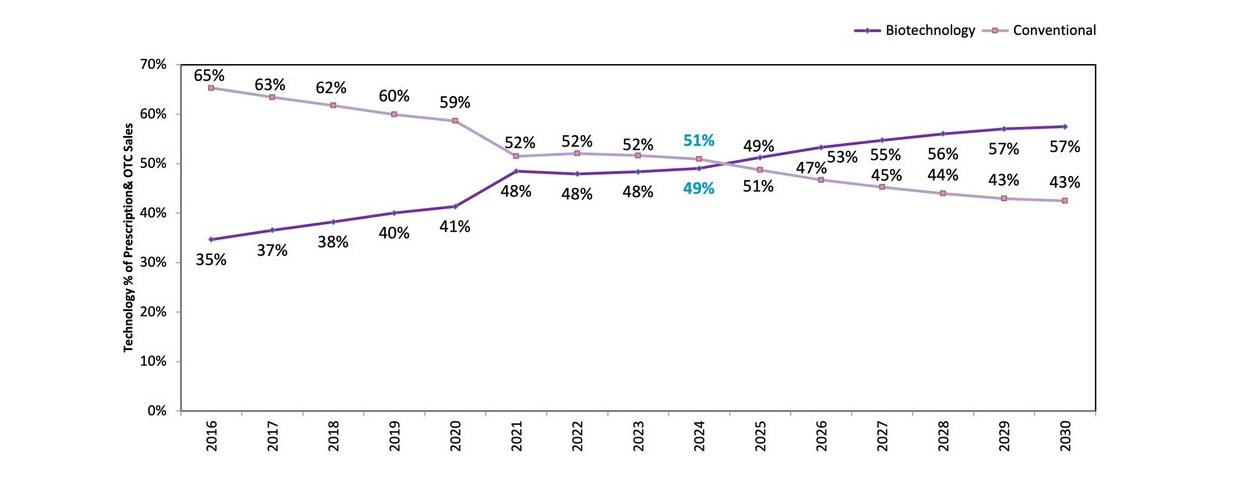

Biologics have, as of 2025, overtaken small molecules in value terms. Large molecule drugs will make up 51% of overall prescription drug value in 2025, rising to 57% in 2030. Over two thirds of the top 100 best sellers in 2030 will be biologics. Few surprises here: biologics tend to command higher prices, and most of the fast-growing new modalities are biologics.

Beware of overlooking small molecules, however. These are still behind the lion’s share of M&A dollars. Pills are convenient, easier to make and cheaper than injections; such considerations are likely to become more important as populations age and cost-of-delivery pressures rise.

Chart 13: Change in sales 2030 vs. 2024 ($bn)

Oral GLP-1s will likely fuel the next sales surge in that sector-leading category. Oral administered drugs are also behind the biggest neurology deals of the last 18 months.

Intra-Cellular’s Caplyta (lumateperone), now part of J&J’s portfolio, modulates the neurotransmitters serotonin, dopamine and glutamate; this triple effect, and the way it modulates dopamine receptors, are what sets it apart from other anti-psychotics. The Karuna drug that BMS paid billions for – since approved for schizophrenia as Cobenfy - is a twice-daily capsule combining a muscarinic cholinergic receptor agonist (xanomeline) with trospium, a compound that blocks those same receptors in the periphery, helping mitigate what would otherwise be uncomfortable GI side-effects. AbbVie’s $8.4 billion Cerevel acquisition came with Parkinson’s hopeful tavapadon, a once-daily partial agonist of certain dopamine receptors.

New technologies can also be used as tools to find better small molecules, rather than as novel modalities themselves. For instance, Light Horse Therapeutics is using CRISPR-based gene-editing to uncover new targets that are druggable using small molecules, rather than to create medicines that directly edit genes. Investors seem to like the idea: Light Horse in January raised a $62 million Series A, one of 2025’s biggest.

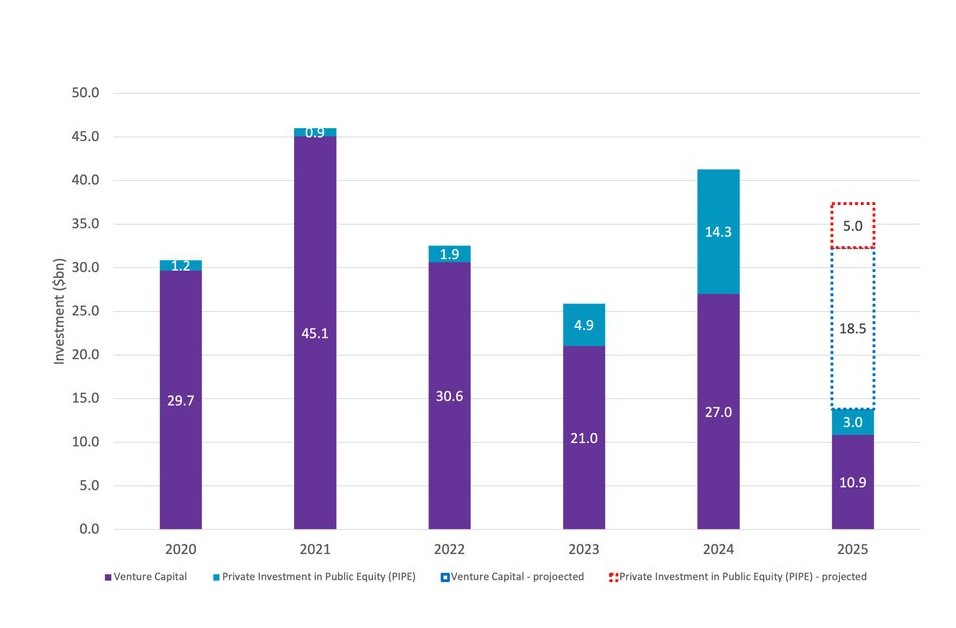

Larger, fewer rounds are a feature of today’s venture landscape. Venture funding totals so far in 2025 look reasonably healthy. But they hide a widening divide between the few biotech “haves”, raising larger rounds, and the many biotech “have-nots”, raising nothing at all.

The “haves” are those with late-stage assets in popular therapy areas, an experienced team, or, more rarely, a promising platform. The have-nots are pre-clinical, data-poor biotechs.

This divide, and investors’ broad retreat from early-stage, novel biology, may – if it endures - damage the health and diversity of the biopharma eco-system.

Chart 14: Worldwide Prescription Drug Sales: Biotech vs. Conventional Technology

Chart 15: Venture Capital and PIPE Deals