Pipelines-in-Products

The next five years could see billions in lost sales as patents expire.

Big Pharma still face over $300 billion in potential lost sales due to patent expiries over the next five years. This represents 3-4% of the overall market, with a bump in 2028 to almost 7% due to Keytruda’s anticipated loss. Merck is hardest hit near term, but AbbVie, J&J, Roche and Bristol Myers Squibb each face over $30 billion in cumulative sales-at-risk by 2030. Few are spared: average cumulative sales-at-risk for the top 25 Pharma firms will approach $24 billion by decade-end.

These figures don’t capture the compensatory impact of up-and-coming drugs, like Merck’s next-generation Keytruda. But they underline the size of the problem and explain why most Big Pharma are nurturing or shopping for sure-bet assets in therapy areas where several chronic disease indications can be squeezed out of a single mechanism.

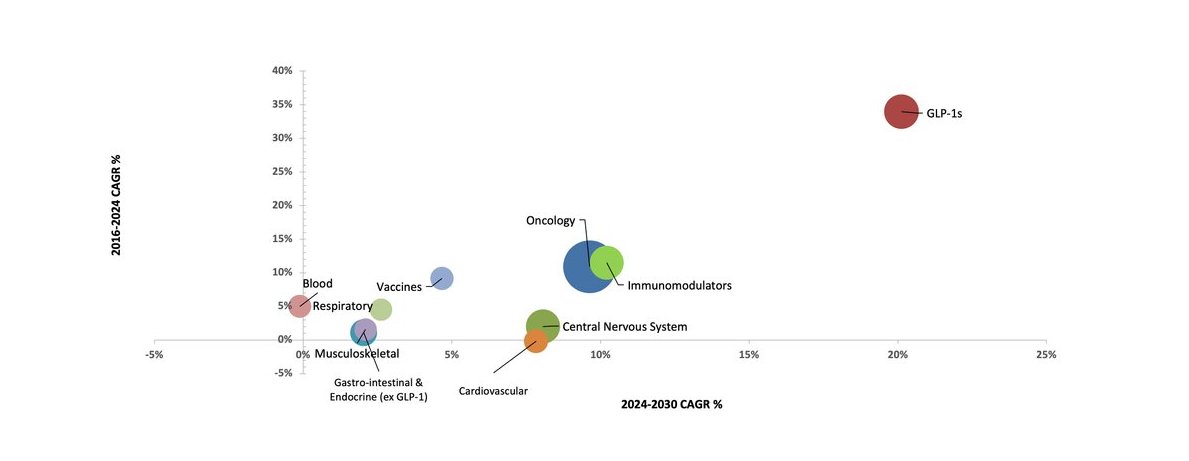

Immuno-inflammation is ripe for such pipeline-in-a-product drugs; immunology is the next-fastest growing field after the runaway GLP-1 engine.

Humira was Exhibit A for multi-indication blockbusters. Modern followers include Sanofi’s Dupixent with 15 approvals spanning asthma to dermatitis, and AbbVie’s Skyrizi, slated to be the world’s second-largest drug in 2030. Skyrizi blocks interleukin-23, an inflammatory cytokine, and can help patients with skin condition plaque psoriasis, the gut disorder Crohn’s disease, and some types of arthritis. It has already notched up four approvals since its 2019 launch. Sales of AbbVie’s second anti-inflammatory, JAK inhibitor Rinvoq (upadacitinib), are forecast to approach $15bn by 2030 across its (currently eight) indications; Rinvoq’s CAGR of over 16% is among the strongest of the non-GLP-1 assets.

Oncology will grow similarly strongly over the rest of the decade. Science took many cancer drugs toward ever narrower, genetically defined indications that proved less commercially attractive. Yet next-generation antibody-drug conjugates (ADCs), bi- and multi-specific antibodies are part of a concerted hunt for more broadly applicable medicines more likely to reach the size of a Keytruda or a Darzalex; the latter, a CD-38 targeted antibody, is approved as part of over half-a-dozen regimens and treatment combinations for multiple myeloma.

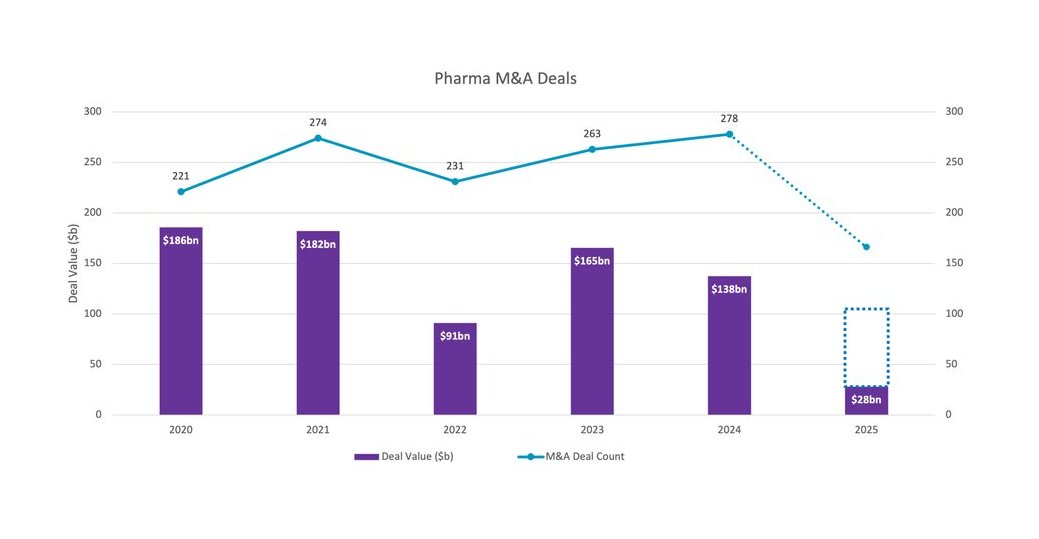

Chart 8: Pharma M&A Deals

The most valuable oncology pipeline contender behind subcutaneous Keytruda is Summit Therapeutics/Akeso’s bispecific VEGF-PD-1 antibody ivonescimab. This dual mechanism drug (which blocks immune evasion and angiogenesis) outdid Keytruda in a head-to-head trial and was approved in China for non-small cell lung cancer in 2024. The candidate is in development for several other cancer types, with peak sales forecasts of $27 billion.

The fastest-growing non-GLP-1 drug is forecast to be Daiichi Sankyo and AstraZeneca’s ADC Enhertu (trastuzumab deruxtecan), whose utility across breast, gastric, lung and other solid tumors puts it on track to top $15 billion in 2030 sales.

Neurology offers similarly large markets and scope for indication expansion. No neurology drugs yet make the top ten most valuable pipeline candidates. But neurology is the fourth fastest-growing therapy area, and a hot dealmaking spot. 2025’s biggest M&A deal so far: Johnson & Johnson’s $14.6 billion acquisition of Intra-Cellular, with its marketed schizophrenia drug Caplyta. Bristol Myers Squibb’s purchase of Karuna (completed in early 2024) and AbbVie’s $8.7 billion Cerevel deal also make the top five biggest M&A since the start of 2024.

M&A is off the pace so far in 2025, as uncertainties around US tariff and drug pricing policy give buyers pause. “I’d be holding off dealmaking for 3-6 months until this [tariff framework] plays out,” said one former Big Pharma CEO in April 2025. The deals that are happening are heavily risk-mitigated. They often involve late-stage or marketed assets, or, if programs aren’t yet over the line, contingent payments.

Merck KGaA’s purchase of SpringWorks came with two on-market rare disease products. GlaxoSmithKline paid $1.2 billion up front for Boston Pharmaceuticals’ Phase 3-ready liver disease drug (targeting FGF21) in May 2025, with a further $800m in success-based milestones. Similarly, Novartis’ $800m deal for Regulus in April 2025 includes a further $900m if farabursen, a micro-RNA-targeted oligonucleotide in mid-stage development for autosomal dominant polycystic kidney disease, is approved.

Deal Completion Date

Acquiring Company

Target Company or Business Unit

Therapy Area

Deal Value ($bn)

April 2025

Johnson & Johnson

Intra-Cellular Therapies

CNS

14.6

March 2024

Bristol Myers Squibb

Karuna Therapeutics

14.0

February 2024

AbbVie

ImmunoGen

Immunotherapy

10.1

August 2024

Cerevel Therap. Holdings

8.7

January 2024

Mirati Therapeutics

Oncology

5.8

May 2024

Vertex Pharmaceuticals

Alpine Immune Sciences

4.9

Gilead Sciences

CymaBay Therapeutics

Liver

4.3

RayzeBio

4.1

Merck KGaA

SpringWorks

Oncology/rare disease

3.9

Eli Lilly

Morphic Therapeutic

3.2