Venture Funding Plummets In Q2 As Mega-Rounds Falter

Mid-Sized Financings Also Dipped

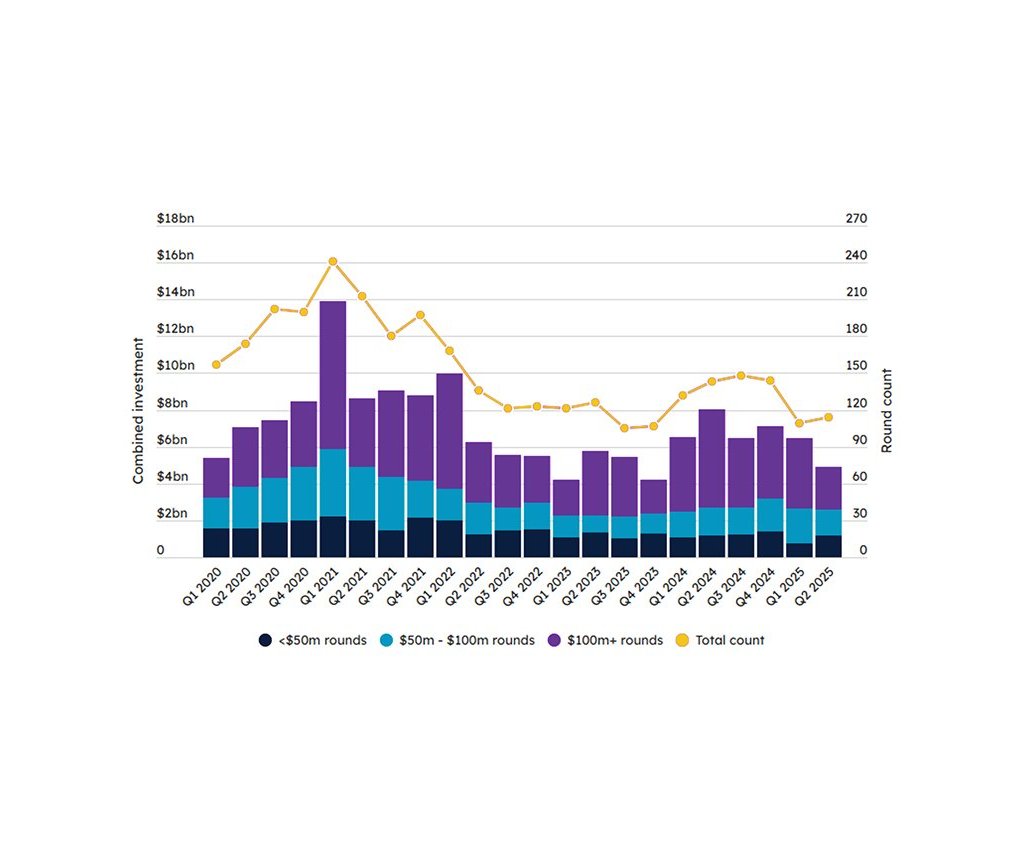

The outlook for biopharmaceutical company financings has grown increasingly grim in 2025 as drug developer valuations remain challenged by various macroeconomic and industry-specific concerns. New data from Evaluate show that the second quarter of this year was particularly harsh for private biopharmas, with venture capital financings down significantly quarter-over-quarter and year-over-year, largely driven by a sharp drop in VC mega-rounds.

Source: Evaluate, Biomedtracker

Evaluate reported that 114 drug developers raised just $4.92bn in venture capital in Q2, down from $6.49bn raised by 110 companies in Q1 of 2025 and $8.08bn raised by 143 companies in Q2 of 2024. The second quarter drop this year is an ongoing decline, since the first quarter fell short of Q4 2024 performance.

It is unclear when financial markets will become more favorable for biopharma firms with tariffs on pharmaceutical products, most favored nation drug pricing and US Food and Drug Administration staffing and policy changes weighing on the industry, but the VC funding trends to date in 2025 are not encouraging for private companies. While financings of $50m or less rose in Q2, the increase was overshadowed by big declines in the $50m-$100m and $100m-plus categories.

Small rounds of $50m or less totaled $1.16bn in the second quarter versus $750m in the first quarter and $1.21bn raised in the second quarter of 2024. Mid-sized rounds in the $50m-$100m range declined to $1.4bn in Q2 of 2025 from $1.91bn in Q1 of this year and $1.49bn in Q2 of 2024, while mega-rounds totaled $2.36bn in Q2, down from $3.83bn in Q1 2025 and $5.35bn in Q2 2024 – a $1.47bn quarter-over-quarter drop and a nearly $3bn year-over-year plunge.

By Evaluate’s count, there were 16 mega-rounds in the second quarter, down from 18 in the first quarter. Also, the top five financings in Q2 were mostly smaller than the top five in Q1, which ranged from $207.5m for Aviceda Therapeutics to $600m for Isomorphic Labs. In Q2, the largest financing was a $365m series D round for Pathos AI in May, but the rest of the top five mega-rounds totaled less than $200m each. Pathos is using its artificial intelligence-based platform to discover and develop oncology medicines.

Antares Therapeutics, spun out of Scorpion Therapeutics after Eli Lilly agreed to buy it for up to $2.5bn in January, launched in June with $177m in series A funding, the second-largest round in the second quarter. Antares will develop Scorpion’s non-PI3Kα precision medicines for cancer and other diseases.

The third place VC round in Q2 was AIRNA Pharmaceuticals’ $155m series B round in April, a significant step up from the company’s series A funding, which started at $30m at launch in 2023 and grew to $90m in 2024. The RNA-editing specialist is using the series B cash to take its lead program, AIR-101 for alpha-1 antitrypsin deficiency (AATD), into the clinic.

Gene therapy specialist Atsena Therapeutics already has its lead program in the clinic, ATSN-201 for X-linked retinoschisis (XLRS), and raised a $150m series C round in April to fund its ongoing Phase I/II clinical trial as well as ongoing preclinical programs. The second quarter’s fourth place mega-round could support ATSN-201 through the current trial’s readout and a US Food and Drug Administration filing.

Azafaros raised the fifth-largest VC round in Q2, bringing in €132m ($142.7m) in May, primarily to fund its lead drug candidate, nizubaglustat for rare lysosomal storage disorders with neurological involvement, such as GM1 and GM2 gangliosidoses and Niemann-Pick disease type C (NPC).

Company

Investment

Financing Round

Specialty

Pathos AI

$365m

Series D

AI-based cancer drug discovery

Antares Therapeutics

$177m

Series A

Precision therapeutics for cancer and other diseases

AIRNA Pharmaceuticals

$155m

Series B

RNA editing medicines

Atsena Therapeutics

$150m

Series C

Gene therapies for retinal diseases

Azafaros

$142.7m

Lysosomal storage disorders

Source: Evaluate, Scrip