Second Quarter M&A Activity Looks Like More Of The Same, Mostly

The biopharma sector booked nearly the same number of acquisitions in each of the past two quarters, according to Evaluate data, but there are some encouraging signs in Q2.

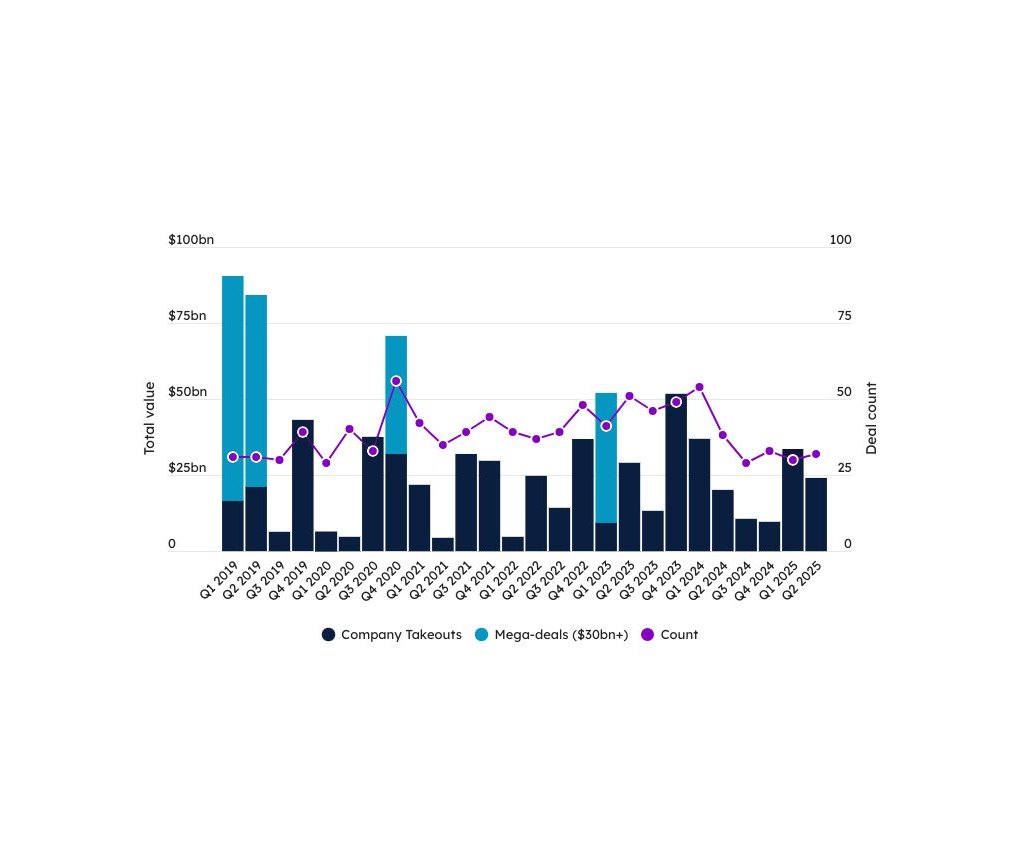

Summer is the time for sequels at the multiplex, and the biopharmaceutical sector offered a remake of its own as many of the datapoints for merger-and-acquisition activity during the second quarter came in similar to Q1 numbers, according to data compiled by Evaluate.

For example:

The industry made 32 acquisitions during Q2, up from 30 in the first quarter.

Each quarter recorded eight acquisitions with total potential value of $1bn or more.

Many of the economic and political uncertainties that have been weighing on dealmaking have remained the same throughout the first half of the year, as the US adjusts to changes under the Trump Administration. However, while marquee deals may be few and far between, attendees at the recent BIO International Convention reported that dealmaking remains active, especially as cash-strapped biotechs seek funding alternatives.

Indeed, the Evaluate data reflects some upticks. There were six M&A deals with upfront value of $1bn or more in the second quarter, compared to just two during Q1. The second-quarter performance continues a recovery from the low points at the end of 2024 and extends a multi-year trend of biopharma companies making bolt-on acquisitions to bolster their pipelines or add platform technologies to their existing capabilities (see table below).

However, the overall value of M&A deals has slipped, with the total potential value for the second quarter’s M&A deals just $23.96bn, down from $33.55bn in Q1.

Source: Evaluate

One key difference between the M&A activity during the two quarters was that the industry seems to gradually be embracing larger upfront commitments. While Sanofi’s $9.5bn takeout of Blueprint Medicines on June 2 was smaller than January’s $14.6bn buyout by Johnson & Johnson of Intra-Cellular, the second quarter saw seven deals in total bigger in total potential value than Q1’s second-largest, GSK’s $1bn acquisition of IDRx.

However, the first quarter produced a higher total upfront value of approximately $16.79bn, nearly 17% higher than the $13.97bn recorded in Q2. Those numbers, however, are skewed by the J&J/Intra-Cellular transaction, which yielded $14.6bn or about 85% of the first quarter’s aggregate upfront value.

The second-quarter numbers represent lower deal volume, but higher deal valuation compared to the one-year-ago activity from Q2 2024, when Evaluate noted 38 M&A transactions with a total potential value of slightly more than $20bn. The past quarter’s 32 deals is a 15.7% volume decline year-over-year, but the Q2 2025 aggregate potential value of nearly $24bn was 19.4% higher than the year-ago total. Q2 2024 also represented a settling of the M&A market, as total deals declined from 54 in the first quarter and total potential value of nearly $37bn.

During Q2 2025, six M&A deals included either upfront cash of $1bn or more or, in the case of not-yet-closed deals, priced based on company valuations of $1bn or greater, up from two in Q1.

The industry seems to gradually be embracing larger upfront commitments.

The apparent willingness of more acquirers to commit upfront prices of $1bn in the second quarter could signal a long-awaited loosening of the purse strings in biopharma M&A, but only the trends and results of future quarters will clarify that.

Leading the second quarter’s deals was the Sanofi/Blueprint takeout, in which the French pharma added to its rare disease portfolio by acquiring Ayvakit/Ayvakyt (avapritinib), the only therapy approved in both the US and EU for advanced and indolent systemic mastocytosis (SM). The agreement included $9.1bn in upfront cash along with a pair of contingent value rights worth $400m tied to the development of oral selective wild-type KIT inhibitor BLU-808.

Purchaser

Acquired

Upfront Value

Date

Sanofi

Blueprint Medicines

$9.5bn

2 June

Merck KGaA

Springworks

$3.9bn

28 April

AbbVie

Capstan Therapeutics

$2.1bn

30 June

Novartis

Regulus Therapeutics

$1.7bn

30 April

Lilly

Verve Therapeutics

$1.3bn

17 June

The quarter’s second-largest M&A transaction saw Germany’s Merck KGaA agree to pay $47 per share, a 24% premium, for cancer-focused SpringWorks. The deal’s estimated total value came to $3.9bn, and Merck KGaA announced that the buyout had closed on July 1. In February, the Connecticut biotech obtained US Food and Drug Administration approval of Gomelki (mirdametinib) for the rare genetic disorder neurofibromatosis type 1 (NF1).

One other M&A deal inked during Q2 brought a price tag above $2bn, as AbbVie agreed to pay $2.1bn on June 30 to acquire early-stage in vivo RNA therapy specialist Capstan Therapeutics. Reportedly, AbbVie’s purchase is motivated both by obtaining Capstan’s proprietary tLNP platform technology designed to deliver RNA payloads, such as mRNA, and CPTX2309, a Phase I anti-CD19 CAR-T candidate for B-cell mediated autoimmune diseases.

Lilly’s June 17 bid of $1bn up front plus up to $300m in CVR payouts to acquire genetic medicine specialist Verve Therapeutics. The two companies had been partnered on PCSK9 base-editing drug development for cardiovascular disease since 2023, and earlier in 2025 selected VERVE-301 as a candidate to advance into the clinic for atherosclerotic cardiovascular disease with high Lp(a).

BioNTech’s June 12 offer to merge with rival German firm CureVac for $1.25bn. The clinical-stage company has been developing mRNA therapeutic candidates for cancer and infectious diseases; CureVac shareholders would retain between a 4% and 6% interest in the merged company under the deal structure proposed by BioNTech.

Shionogi’s agreement on May 7 to acquire two pharmaceutical-focused subsidiaries of fellow Japanese company Japan Tobacco – Torri Pharmaceutical and Akros Pharma – for about $1.05bn. Shionogi characterized the deal as an effort to gain share of voice in the hospital sales sector in Japan and to strengthen its manufacturing capabilities.