Case study

Learning from AbbVie’s patent cliff pivot

While our attention is on the patent cliff beginning in 2025, this decade has already seen the tangible impact of a major loss of exclusivity and how the originator strategically responded to mitigate the effect. This, of course, is Humira, where AbbVie’s proactive, multi-pronged approach to reducing dependence on its flagship product serves as a compelling case study. AbbVie’s success in navigating such a significant inflection point in the company’s trajectory underscores the value of thoughtful portfolio diversification and forward planning.

In line with many pharmas facing a growth gap and a patent cliff, AbbVie turned to forward-looking M&A to cushion the financial impact of Humira’s sales erosion. The most prominent move came in 2019 with its mega-merger with Allergan. At the time, this was a transformative deal that not only injected substantial new revenue into AbbVie’s portfolio, but also broadened its therapeutic footprint across immunology, neuroscience, and oncology. Leading products such as Botox and Vraylar played a central role in this diversification effort. As Humira reached its loss of exclusivity, AbbVie further reinforced its pipeline through the narrower, strategic acquisitions of Cerevel Therapeutics and ImmunoGen, strengthening its position in key growth areas and underscoring its commitment to long-term innovation and resilience.

Aside from M&A, AbbVie’s strategic maneuvering around Humira’s patent expiry offers a textbook example of how pharmaceutical firms can further mitigate the impact of loss of exclusivity. From patent thickets to biosimilar settlement agreements, AbbVie both delayed and staggered the onset of end-of-lifecycle competition. While the exact playbook may not be reproducible today, the net result bought the company considerable time to develop the clinical profiles of its next-gen immunology brands Rinvoq and Skyrizi.

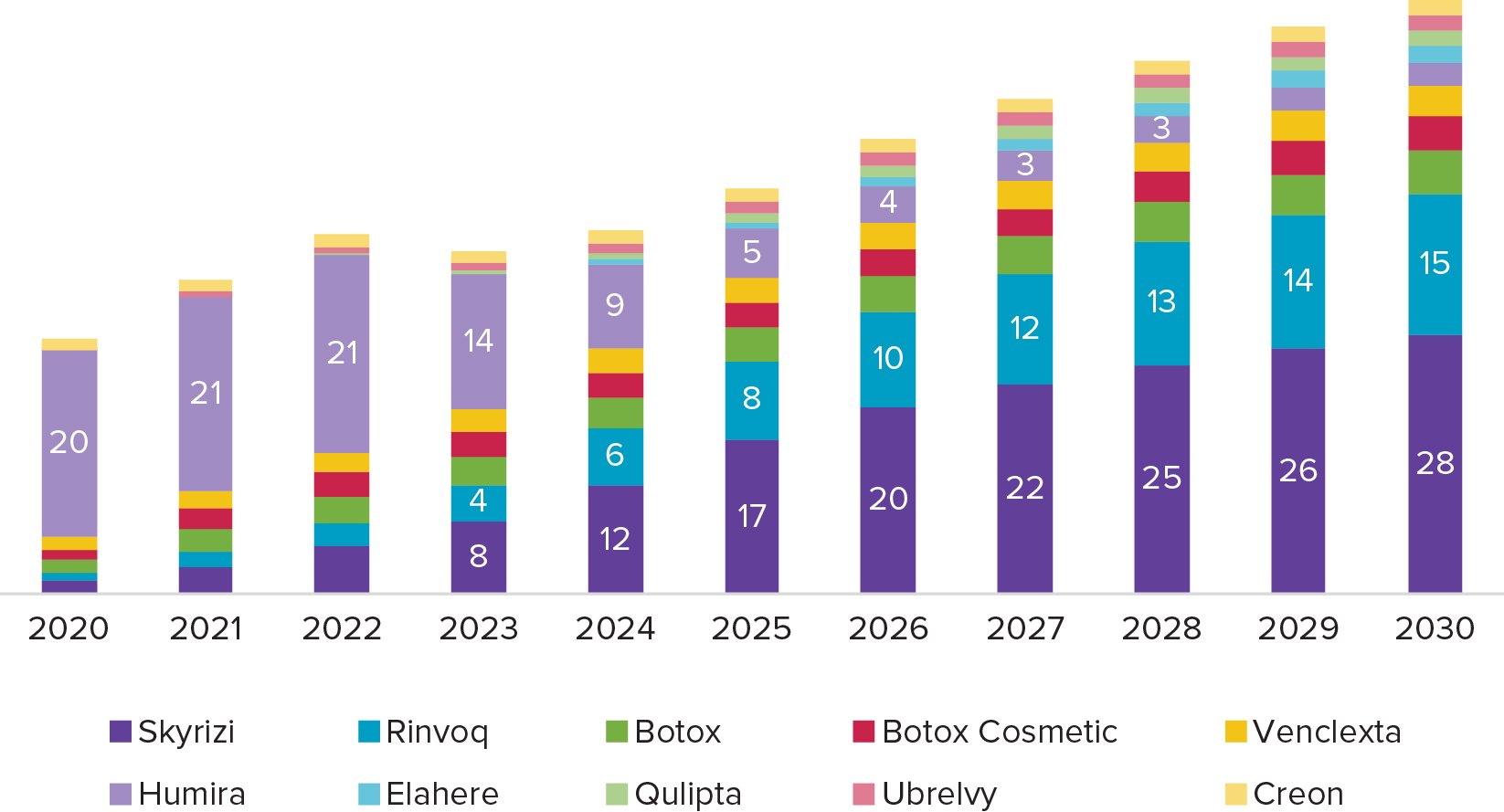

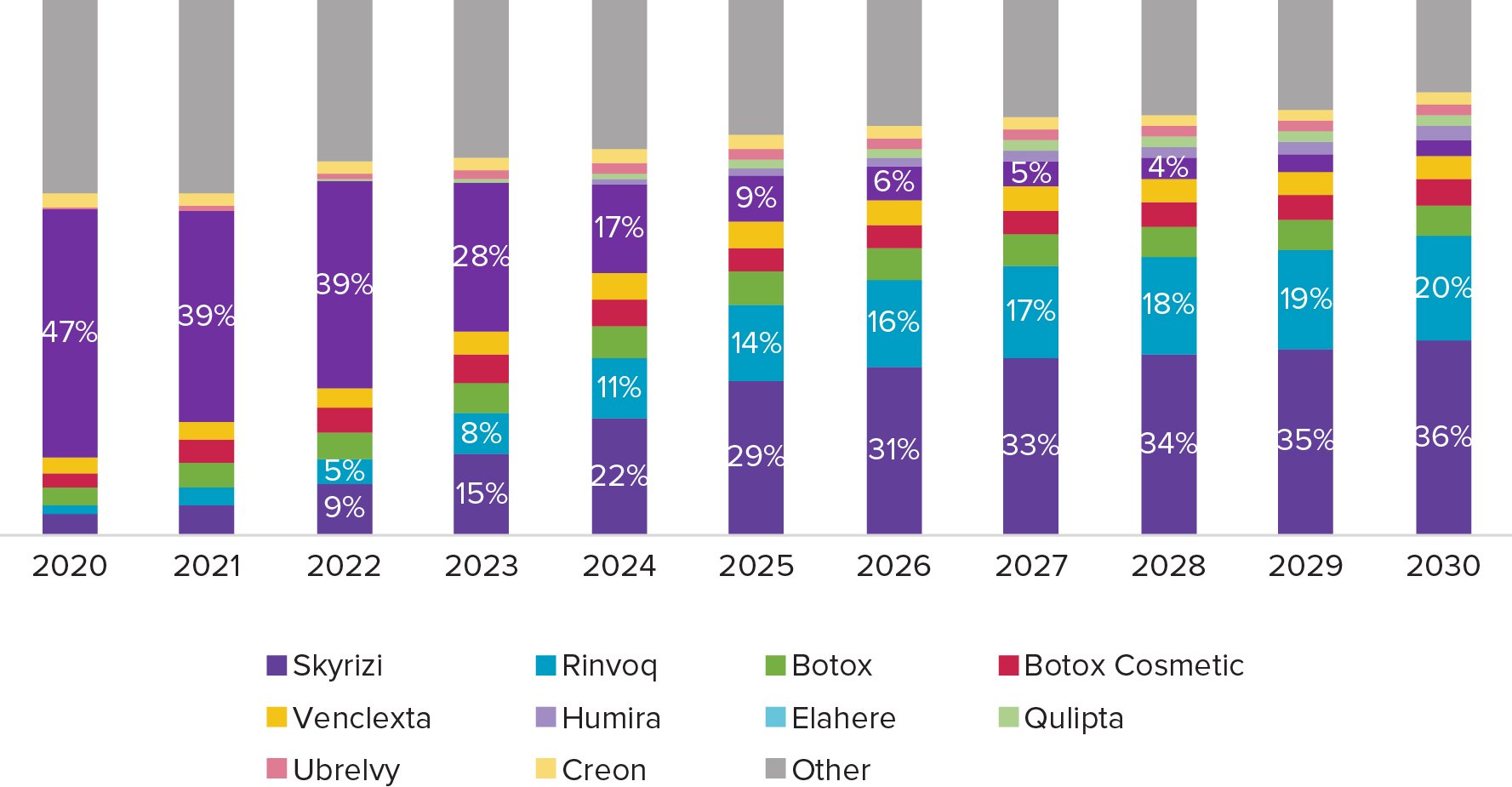

Accordingly, by January 2023, when Humira faced biosimilar competition in the US, these new products had already become the new standard of care in a range of treatment settings. So as Humira began its decline, Rinvoq and Skyrizi were not only strong growth drivers, but also meaningful revenue contributors. AbbVie had successfully tapered its reliance on Humira: from 39% of revenues in 2022 to 9% expected in 2025, while the next-gen is rising from 14% to 43% in the same period.

Between the asset reprioritization within AbbVie’s immunology portfolio, and momentum provided by acquisitions, the company’s patent cliff is now firmly in the past. Rather, AbbVie has a clear window and multiple strong, diversified growth drivers. And compared to its peers, its growth gap is the smallest of any large pharma company that isn’t called Eli Lilly or Novo Nordisk. This deliberate rebalancing shows the success of AbbVie’s strategy in managing lifecycle risk and sustaining growth amid the loss of exclusivity for a once-time best-selling drug.

Figure 5. AbbVie’s top 10 branded products by WW sales ($bn)

Source: Evaluate Pharma

Figure 6. AbbVie’s total revenue split by top 10 products