Strategy archetypes for managing patent cliff

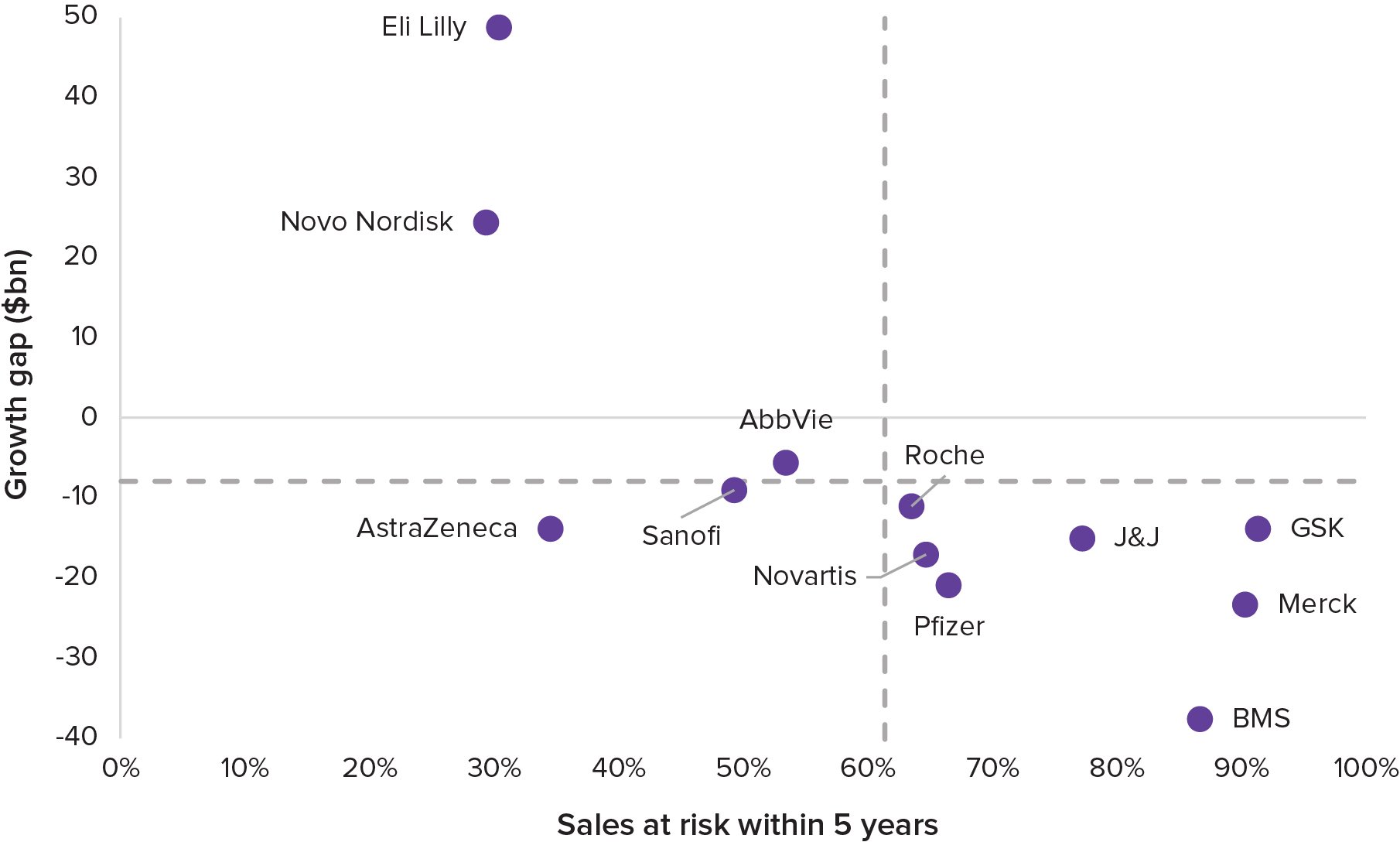

Our next analysis takes the growth gaps for each large pharma company and plots against their exposure to the upcoming patent cliff. While these two metrics are certainly related, they are not completely dependent on each other.

You can imagine each company oscillating anticlockwise around the chart as their portfolio matures and is refreshed, like socks on an extremely low spin cycle. Ideally portfolio strategists are targeting the upper left quadrant and minimizing the duration spent in the bottom right, avoiding extreme swings relative to their peers. The dotted lines denote the peer-set averages for growth gaps and patent risk.

It is through the respective positioning of each company that we can contextualize their recent portfolio and business development decisions. From this we have created a set of strategy archetypes for how large pharma goes about managing patent cliffs, and how successful these have been.

Figure 4. Large pharma sales risk vs growth gap

Source: Evaluate Pharma

This is the ultimate position of luxury, whereby growth drivers and limited patent cliff exposure coalesce. The challenge that such companies face is investing in future-proofing in such a way that adds greater value than any immediate measures such as share buybacks. Many companies have struggled to find repeat success after a windfall, such as reinvestment of COVID-19 revenues or Gilead’s pivot towards oncology that followed its accomplishments in hepatitis C.

Predictably, Eli Lilly and Novo Nordisk both find themselves in this situation today. The scale of their GLP-1 market positions will afford them more tactical freedom than any other biopharma company that has preceded them, but they should be mindful of Gilead’s previous experience and overdiversification. It has taken Gilead a decade to reclaim its prior status, largely thanks to its HIV strategy and continued focus on renal diseases.

Both Lilly and Novo Nordisk are continuing to make long-term bets to secure their GLP-1 and associated cardiometabolic franchises. This includes asset-driven deals to fill pipeline gaps, in addition to longer-term discovery alliances centered on novel modalities. The temptation to enter entirely new, unrelated therapy areas will be great, but a cautious and staggered approach is advisable.

AbbVie also just squeezes into this demographic, and we will explore how it has achieved this position despite not yet being involved in the GLP-1 market in a case study towards the end of this report. But its future strategy will likely bear closer resemblance to those in the bottom left quadrant.

This is the ultimate position of luxury, whereby growth drivers and limited patent cliff exposure coalesce.

A low patent risk meets a gentle need to supplement the pipeline. Companies meeting these criteria typically have operational freedom to cherry-pick the right company or drug, at the right valuation. A longer-term view allows large pharma to assume an element of clinical or commercial risk that is balanced by upside potential, and mitigated through completing numerous such bolt-on deals.

Ideal strategies here include adding de-risked late-stage or commercially available drugs that have strong portfolio synergy. Companies such as AstraZeneca and Sanofi in this quadrant are still looking for new revenue drivers, despite having a smaller growth gap than some of their peers. And Sanofi’s acquisition of Blueprint is a prime example of a deal with a near-term payoff, while AstraZeneca’s rumored interest in Summit Therapeutics has a strong rationale.

Bolt-on deals have been in favor so far this decade as patent risk has generally been low. But as the patent cliff approaches and intensifies, the likelihood of larger deals and major consolidation grows. This leads to the third quadrant.

Companies in this quadrant face the greatest challenge. However, the huge overperformance of Eli Lilly and Novo Nordisk distorts the average growth gap, meaning that some large pharmas may rightly grumble at finding themselves in this grouping.

Nevertheless, these companies face higher than average growth gaps and greater patent cliff exposure, which is a dangerous combination. Ideally these companies can improve their position on both of these metrics by adding meaningful and youthful revenue streams. The problem is that acquirable companies that fit this profile are rare commodities, and factoring in the right price and portfolio synergy is a goldilocks scenario. This leads to intense competition and lofty premiums, which can stretch deal rationale to the brink. Anecdotally, Amgen’s acquisition of Horizon (ahead of Sanofi and J&J) fits the bill and the combined company is now more youthful with growth prospects.

The further from the center point the large pharma is, the more urgent the need – and therefore the weaker the negotiation position. Failure to act with precision and urgency can see a company's fortunes spiral out of control whereby cycles of commercial underperformance and cost-cutting follow each other. Thankfully there aren’t any real examples of fallen star pharmas in the current environment, as smart portfolio decision making and reinvestment in R&D has allowed the rejuvenation of companies that may have fit the bill previously. This is the situation that BMS is facing most acutely, alongside Bayer – now slightly out of large pharma scope.

Growth in spite of a patent cliff indicates that the underlying portfolio engine is very strong. The scenario facing companies here is to refocus and reprioritize resources around these growth drivers and slim down elsewhere. Executing this transition while minimizing disruption to the wider business is key; this is less of a portfolio venture – existing products that drag on growth and profitability are obvious – but rather an exercise in change management.

That no company finds themselves in this quadrant is indicative of the recent M&A environment, which has strongly favored smaller deals compared to larger mergers. BMS in the years following the Celgene acquisition is perhaps the prototypical company – its patent cliff was still hugely influential, although Revlimid’s growth bought the company additional time with which to continue its pivot. As it turned out, a succession of pipeline failures and the slow CAR-T market caused BMS to slip backwards.

GSK is the closest present-day company to this situation. Its patent cliff exposure is the highest among peers at ~90%, although this is being managed through a pivot towards oncology, while rejuvenating its longstanding respiratory and infectious disease franchises. Furthermore, the divestment of its consumer health business has provided the strategic focus and financial capability to invest in this transition.