The leading culprits

The list of brands facing patent expiry of loss of exclusivity in the next six years is extensive. Evaluate’s database contains more than 400 such drugs, although their relative impact is widely variable. Focusing on the main contributors to the industry-wide patent cliff, 68 separate products will be blockbusters at the time of expiry. Exactly half of these will generate more than $2bn in annual sales, while the ten biggest expiries share $126bn in at-risk revenues. These are outlined in the table below.

68 separate products will be blockbusters at the time of expiry.

Table 1: Top ten expiries during the 2025–30 patent cliff

Drug

Company

Major patent expiry or loss of exclusivity

Prior year sales

Portfolio contribution

Keytruda

Merck

Dec 2028

$32.6bn

53%

Darzalex

J&J

May 2029

$17.8bn

27%

Eliquis

Bristol Myers Squibb

Nov 2026

$14.3bn

31%

Jardiance

Boehringer Ingelheim

Aug 2028

$11.8bn

51%

Ocrevus

Roche

Mar 2029

$9.9bn

15%

Opdivo

$9.2bn

22%

Vabysmo

Mar 2030

$8.9bn

13%

Cosentyx

Novartis

Dec 2029

$8.3bn

14%

Gardasil 9

Jun 2028

$6.8bn

11%

Prevnar 13

Pfizer

Dec 2026

$6.4bn

Source: Evaluate Pharma

The leading culprits are primarily diffused among large pharmaceutical companies. Merck and Bristol Myers Squibb are doubly exposed, both having two products in the top ten that combine for 64% and 54% of their portfolios, respectively. The similarities don’t end there, as their positions are driven by the end of a prolonged period of success in the PD-1 antibody market.

Patent cliffs and slower growth go hand in hand. And with this patent cliff disproportionately affecting large pharma, it is also these companies that will see slower growth.

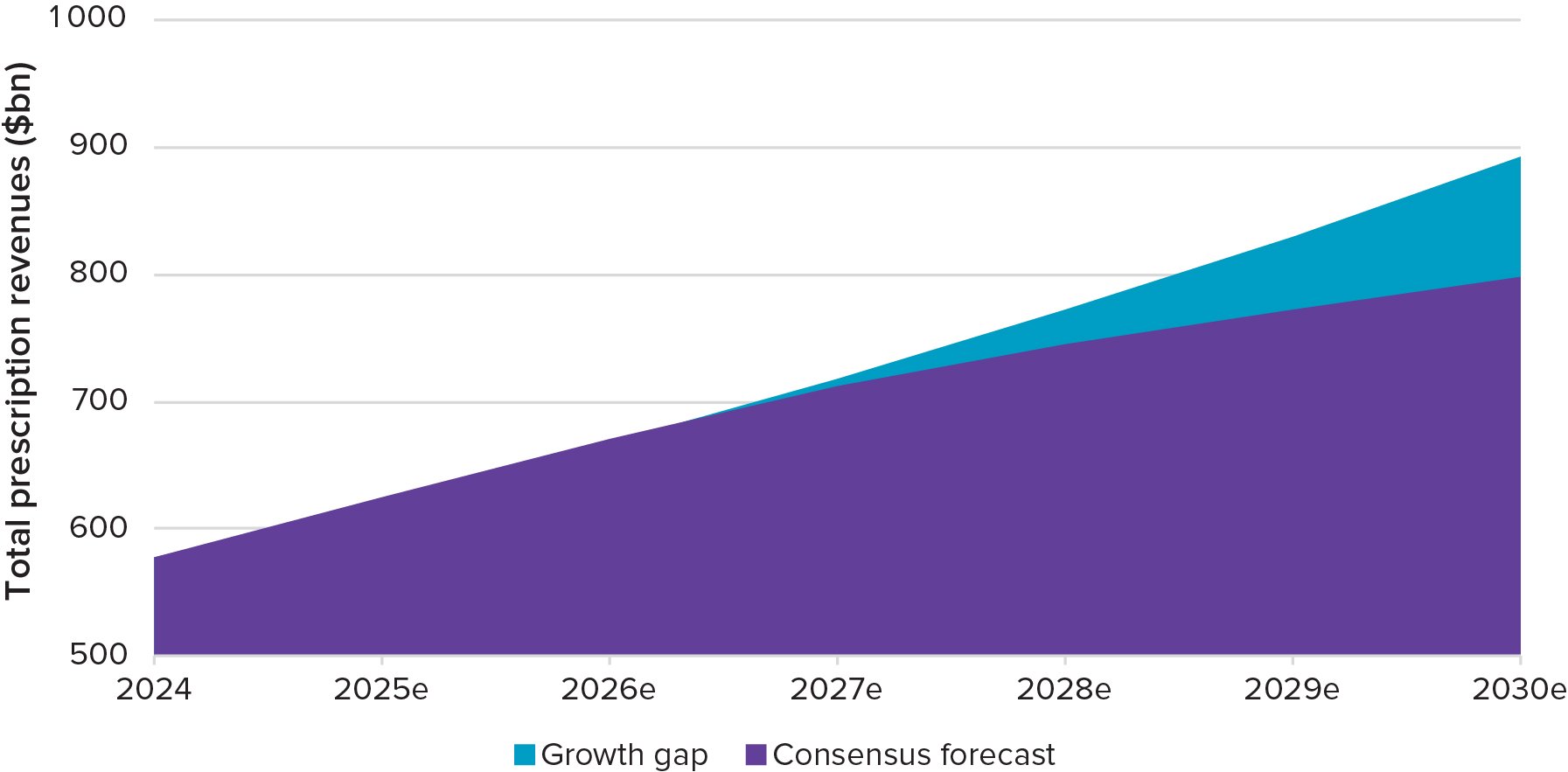

Using a method inspired by EY’s analysis in its Biotech Beyond Borders report, Evaluate calculates that large pharma’s growth gap sits at $94bn by 2030 revenues. This is the difference between current analyst consensus for these companies, and the hypothetical scenario by which each company is able to grow at a market-average CAGR. This excludes COVID-19 products due to their one-time distortion effects, and is set at 7.5%.

Evaluate calculates that large pharma’s growth gap sits at $94bn by 2030 revenues.

Pharma companies are constantly striving to replenish revenues of mature, expiring drugs with their new launches. But it is clear that current portfolios will be insufficient, especially amidst a significant patent cliff. A simplistic view suggests that pharma companies will turn to external deal-making in order to source a large portion of the almost twelve-figure growth gap.

Figure 2. Large pharma’s growth gap to 2030

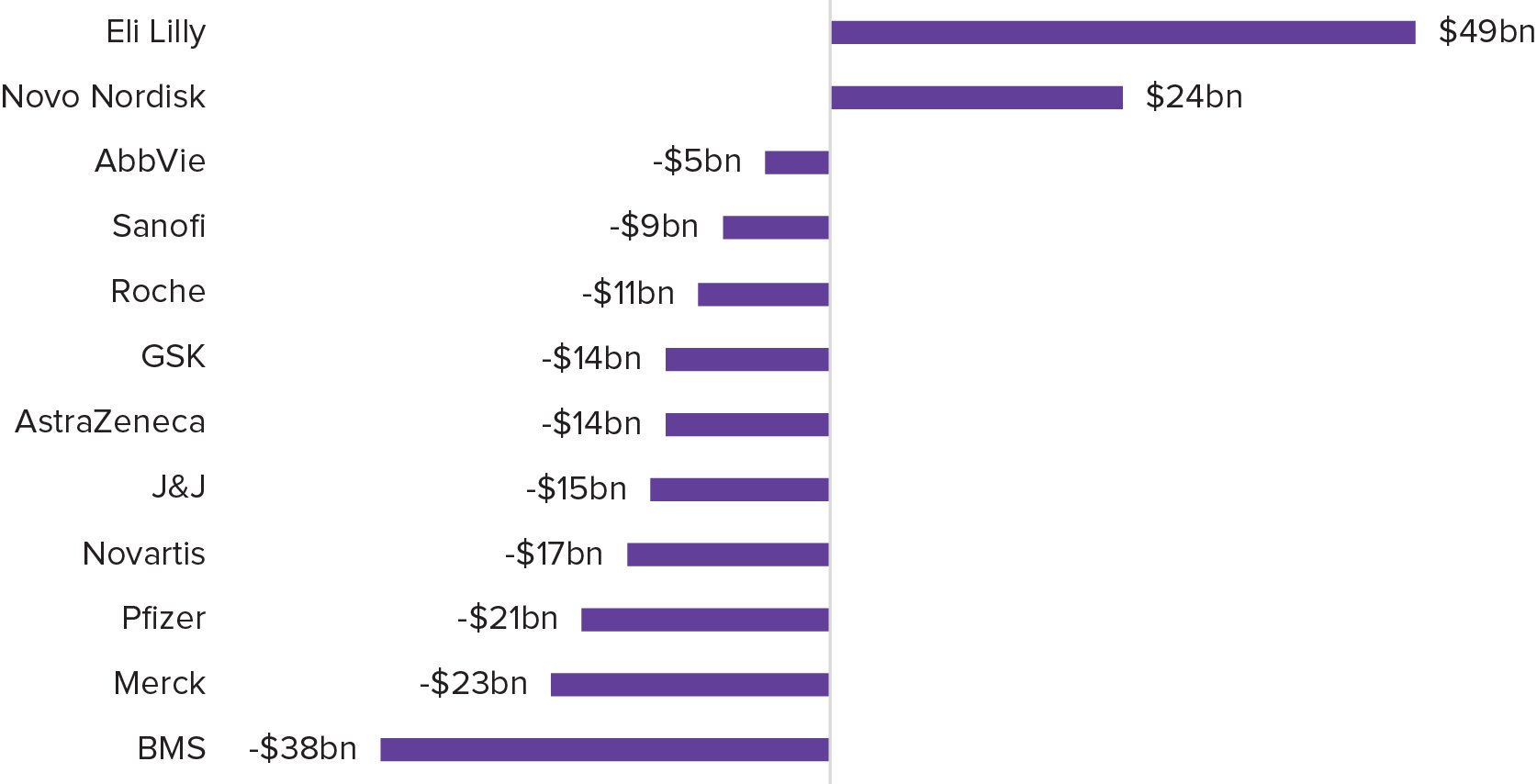

There are 12 companies making up our definition of large pharma in this report, each with 2024 revenues of around $40bn or greater. The chart below shows how they fare against each other in terms of their own individual growth gaps. A clear separation emerges between a select group of overperformers and those needing to build new growth drivers.

Figure 3. Individual growth gaps within large pharma

As expected, Eli Lilly and Novo Nordisk will ride the GLP-1 wave for the rest of this decade. Astonishingly, Lilly is expected to produce almost $50bn in sales above-and-beyond an average growth rate by 2030. It is their successes that exacerbate the situation facing their non-GLP-1 peers. Their lack of participation in this unique market leaves the need to identify alternatives – and potentially several of them – in order to achieve a 7%+ CAGR.

Within this group of “have-nots”, BMS faces the largest growth gap by far. The company has the dual challenge of an underperforming late-stage and launch portfolio, combined with one of the largest patent cliffs. Here it joins Merck and Pfizer – and it is not a coincidence that these three companies have been among the most acquisitive so far this decade. Note that at the time of writing, Merck’s $10bn deal with Verona has not yet concluded, which would shrink Merck’s gap by around $1.5bn in 2030 revenues. Similarly, Sanofi’s buyout of Blueprint Medicines is not yet included ($2.0bn in 2030).

Of the companies in the middle ground, AstraZeneca is an interesting case study. Its leadership has often spoken of an $80bn revenue target by 2030, having achieved an ambitious transformation after fending off a potential acquisition by Pfizer. The gap between Evaluate’s current consensus for AstraZeneca and this $80bn target is $15bn, which is nearly identical to our calculated growth gap of $14bn. In our view, this validates the growth gap analysis and indicates that large pharma leadership views 7%+ CAGR as an achievable goal, even without meaningful participation in the GLP-1 market.