In a buyer’s market, pharma carves out assets and contingencies

For biotech investors willing to stay the course, carve-out deals offer an alternative to dilutive funding rounds.

In a buyers’ market, what pharma wants, pharma gets – a mantra that applies to the assets themselves, and how they’re paid for.

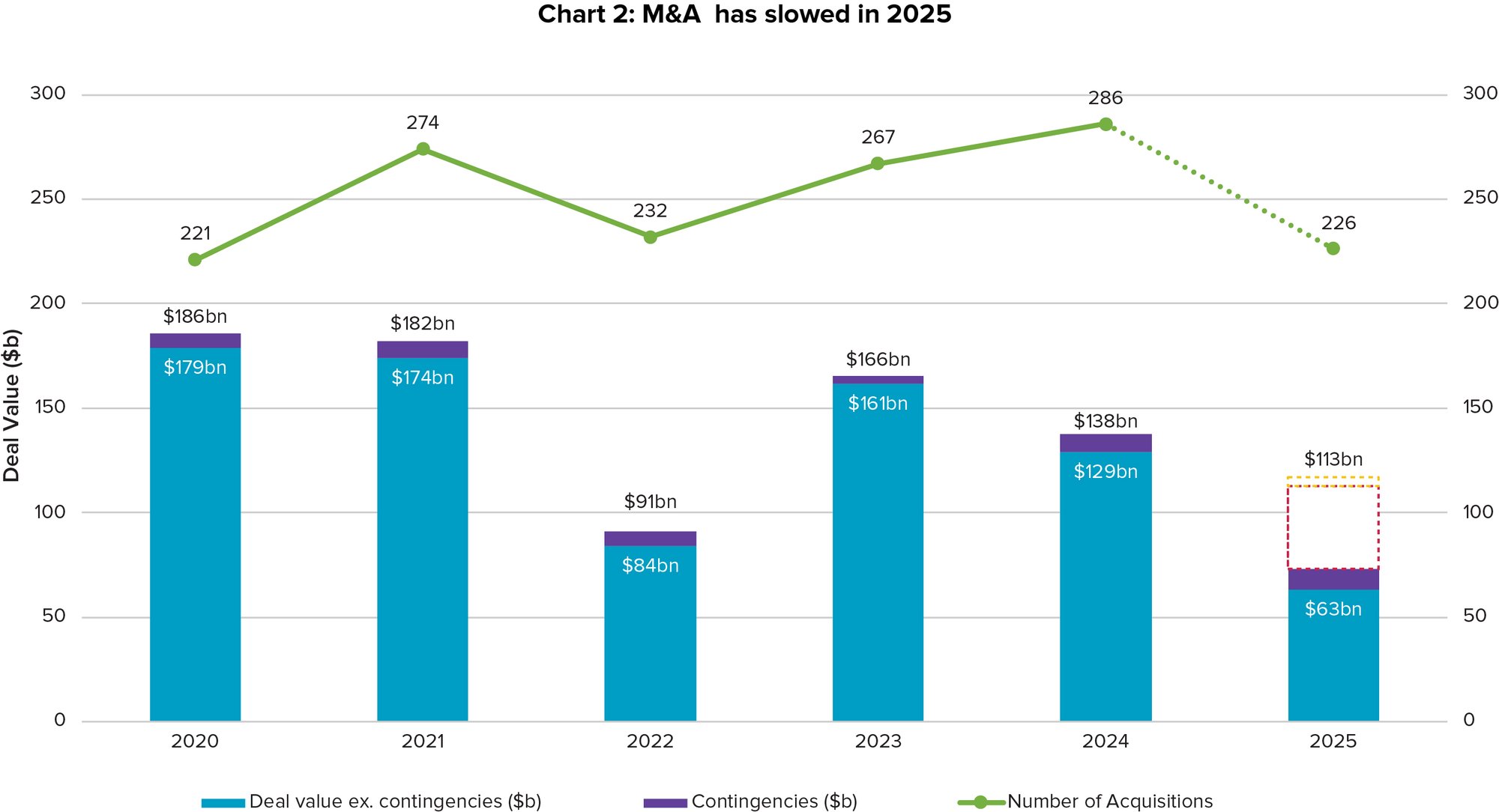

These days, many pharma firms want commercial or late-stage drugs to quickly fill large loss-of-exclusivity revenue gaps; pharma could face $300 billion in potential lost sales this decade according to Evaluate forecasts. Yet Big Pharma have also sought to minimize risk in the face of the Trump Administration’s see-sawing tariff and investment policies, uncertain global economics, and a skittish US competition authority.

The result: fewer ‘mega-deals’ in the 24 months or so since Pfizer’s $43 billion acquisition of Seagen (see Chart 2). Instead, a handful of mid-sized deals and flurries of targeted, bolt-on transactions in the $1-5 billion range to beef out strategic franchises.

Carve-outs are a popular format. Pharma typically seeks assets rather than entire companies (unless they’re also after a new platform technology). In 2022, Pfizer didn’t want all of BioHaven; it wanted the company’s marketed migraine drug Nurtec ODT and related calcitonin gene-related peptide (CGRP)-based assets. As part of the $11.6 billion deal, BioHaven’s remaining assets were assembled into newly created Biohaven Ltd.; that company is currently awaiting FDA approval of spinocerebellar ataxia candidate trorilozole.

For biotech investors willing to stay the course, carve-out deals offer an alternative to dilutive funding rounds. Numab sold its Phase 2-ready anti-inflammatory bispecific antibody to J&J in 2024, packaging it into custom-made “Yellow Jersey Therapeutics” and charging $1.25 billion. “We knew it was a big program that would require significant capital,” recalls Naveed Siddiqi, partner at Novo Ventures. Investors were willing to fund more data, he says, but J&J – with eyes on not just atopic dermatitis, but other inflammatory skin diseases – made an attractive offer.

Sanofi in early 2025 was similarly keen on a Phase 1 myeloid cell engager which it plucked from Dren Bio’s pipeline via a newly created affiliate, paying $600 million up-front. Private Dren Bio – whose most advanced asset is in Phase 2 for certain blood cancers – gets cash to help advance its pipeline (including, possibly, up to $1.3 billion in development and launch milestones). Sanofi gets full control of a strategic asset to boost its immunology pipeline and protects its profit and loss (since acquisitions are typically recorded on the balance sheet, unlike regular licensing deals which are usually expensed to the P&L).

Eli Lilly’s cancer-focused asset carve-out deal with Scorpion Therapeutics in January 2025 and AbbVie’s $1.2 billion acquisition of Gilgamesh’s Phase 2 psychedelic bretisilocin in August 2025 follow a similar template. The buyers get only what they want, leaving biotech teams and their investors a chance to go again.

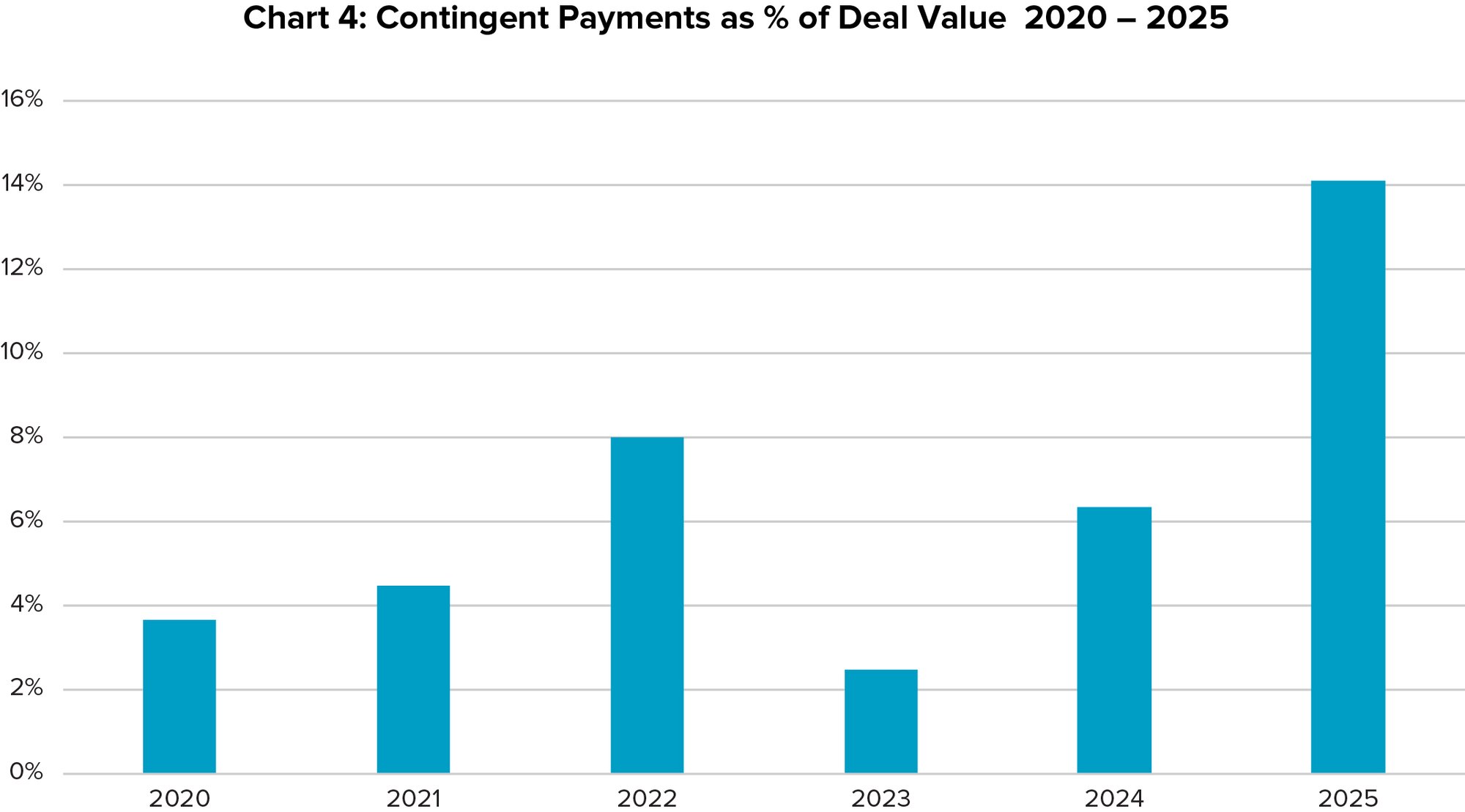

Contingent payments are another popular feature across 2025 transactions (see chart 4). Such payments comprise over 14% of overall M&A value in 2025 so far, more than three times the shares seen in 2020 and 2021.

Roche’s September 2025 deal for 89bio and its Phase 3 metabolic dysfunction-associated steatohepatitis (MASH) candidate pegozafermin (which originated at Teva) comprised $2.4 billion up-front and a further $1.1 billion in commercial milestones.

Novartis’ April 2025 deal for publicly-traded Regulus and its oligonucleotide-based kidney disease candidate farabursen involved $800 million upfront, with a further $900 million owed to Regulus shareholders if the drug – which had completed Phase 1b trials at the time of the deal – meets a future regulatory milestone (e.g. approval). It’s a right-to-buy at a pre-agreed price that would have been higher than $1.7 billion had the Swiss group waited. Novartis’ $925m Anthos deal, similarly, comes with a further $2.15bn in milestones to Anthos’ shareholders (which include Blackstone and Novo Holdings) if the asset – which has Fast Track status and is the subject of three Phase 3 trials – is approved and sells.

Table 1: Top 2025 M&A Deals by Deal Value

M&A Deal Date

Acquiring Company

Target Company or Business Unit

M&A Deal Status

Deal Value ($bn)

Upfront Value ($bn)

April

Johnson & Johnson

Intra-Cellular Therapies

Closed

14.6

-

July

Merck & Co

Verona Pharma

Open

10

Sanofi

Blueprint Medicines

9.5

9.1

Sep

Pfizer

Metsera

7.2

4.9

Sept

Roche

89Bio

3.5

2.4

Merck KGaA

SpringWorks Therapeutics

3.4

Novartis

Anthos Therapeutics

3.8

0.9

Consortium of Investors

Bavarian Nordic

3

Aug

AbbVie

Capstan Therapeutics

2.1

Vicebio

1.6

1.15

In this risk-off, buyers’ market, a relatively high share of M&A value among biopharma dealmakers is contingent on certain milestones.

These days, many buyers want to see more than just an approvable drug. They want to see whether – and how fast – it sells. Hence deals like Merck’s $10 billion acquisition of Verona Pharma, which came almost a year after FDA approval of chronic obstructive pulmonary disease drug Ohtuvayre (ensifentrine), and after the biotech firm had executed a strong launch. Johnson & Johnson in early 2025 paid $14.6 billion for IntraCellular nearly five years after the launch of schizophrenia Caplyta.

It was a similar story mid-year for Sanofi and Blueprint Medicines, whose rare immunology drug avapritinib (Akayvit) got to market in 2020, with follow-on indications approved in 2021 and 2023. (That $9.1 billion deal also came with $400m in milestones related to a pipeline asset.)