Introduction

Biotech is being whipped into shape faster than pharma.

Four years post-pandemic, the doom vocabulary applies more obviously to biotech than Big Pharma. Flaky public markets, choosy venture capitalists, risk-shy buyers: these challenges afflict the smaller, pre-revenue drug-hunters.

Yet Big Pharma is also under pressure. Rising R&D costs, unpredictable regulators, multiplying price curbs and a quicksand policy environment are forcing new rounds of cost-cutting and pipeline trimming.

Meanwhile, China’s fast-growing, ultra-efficient R&D machine is churning out licensable assets that may undercut Western counterparts of all sizes. Pharma firms are snapping up many of these programs today, but the longer-term consequences of China’s rise are less clear. Will it erode early-stage innovation in the West, or just make scientists more secretive? Will it weaken the global discovery and development eco-system, or provide competition that raises standards throughout?

Biotech is being whipped into shape faster than pharma. Its smaller, more fragile organizations have suffered the most extreme natural selection: pre-downturn, the sector counted almost 900 public biotechs. That figure is now barely above 700. New financial entities are being set up to extract funds trapped within dozens of listed biotechs trading at below-cash levels.

Yet biotech’s overhaul provides lessons for pharma about capital efficiency, focus and adaptability – lessons that are more pertinent today than ever before. Drug pricing pressure is already forcing pharma to cut R&D and open new sales channels; it’s also nudging developers to prioritize affordability and convenience over novelty.

Today’s unique mix of challenge and change is blurring (already blurry) boundaries between biotech and pharma. (Gilead is already worth more than Sanofi, and Vertex is more valuable than GlaxoSmithKline.) Many survivors among new-generation biotech – the “haves” able to lure investors – are fattening out into commercial organizations, while pharma slim down and outsource. Bristol Myers Squibb in July 2025 spun off five early-stage immunology assets into a new company funded by asset manager Bain Capital. A new biotech from veteran leaders John Maraganore and Clive Meanwell is chasing not novel targets or ligand design, but an all-in-one injection for lowering heart disease risk that may be sold direct-to-consumer.

Rules and roles across biopharma and healthcare are changing. (See box below)

Pharma opens direct-to-customer sales channels

Biotechs shift downstream into commercialization

Asset managers and private equity join VCs as biotech investors, widening financing options

Pharmacy benefit managers/insurers challenged by price-transparent upstarts, tech-enabled platforms and pharma direct-to-consumer efforts

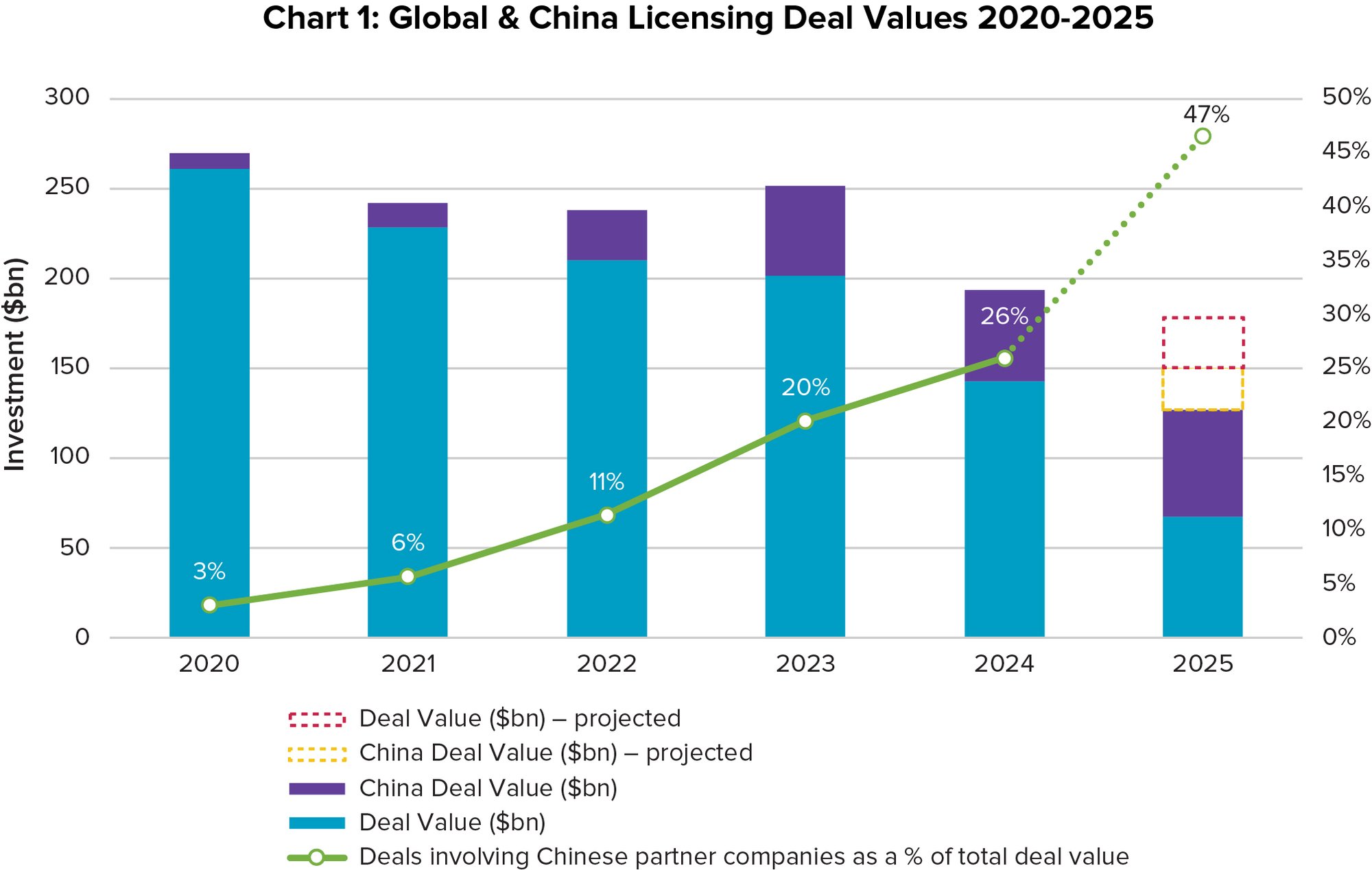

China’s biopharma sector rises to challenge Western dominance (see chart 1)

China’s rapid and increasingly high-quality drug development is a wake-up call to Western biopharma, already suffering from unsustainably low R&D productivity. Assets emerging from Chinese scientists’ engineering prowess, work ethic, and access to trial patients at the country’s vast clinical centers are quickly permeating Western dealmaking and pipelines. China-sourced assets are forecast to comprise close to half of 2025’s overall licensing deal value; they are also filling new, Western-VC-funded start-ups like Braveheart Bio (CV diseases) and Ollin Biosciences (ophthalmology).