Trends by Asset Target

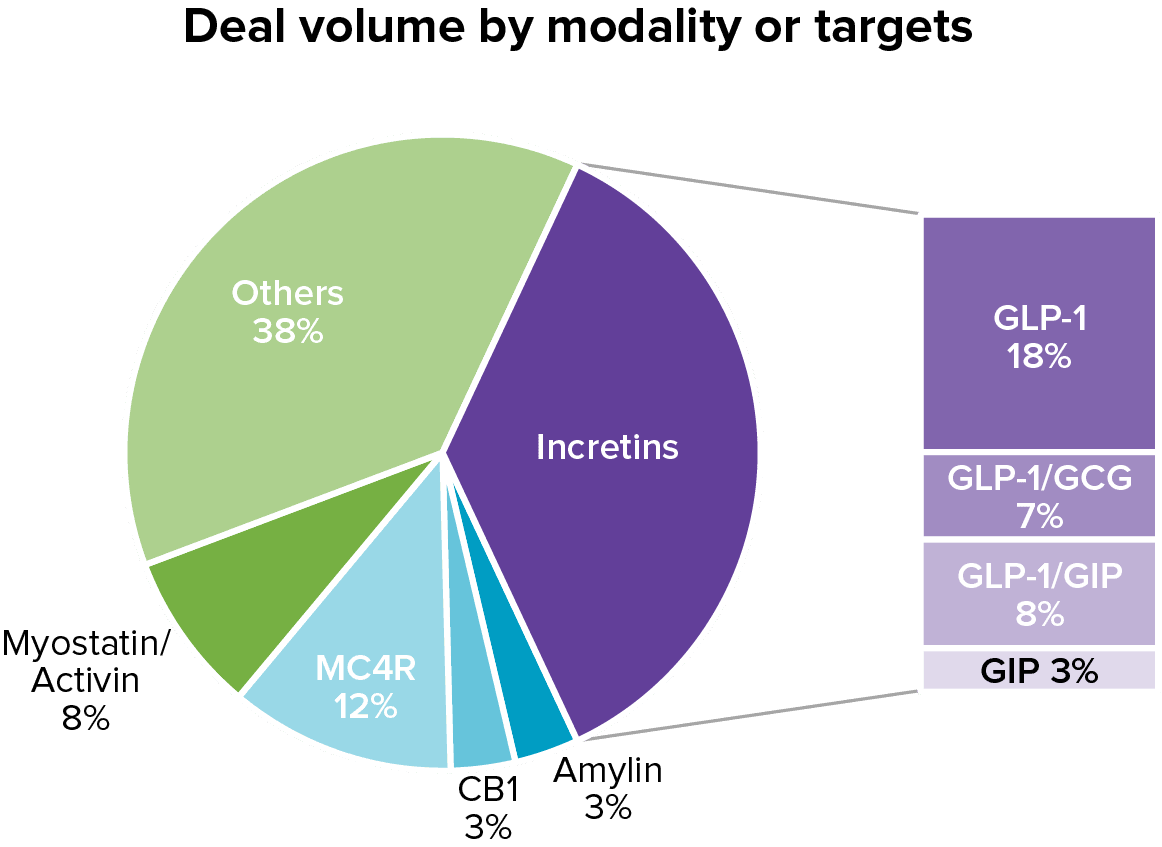

GLP-1 remains the dominant target in obesity dealmaking, but diversification is accelerating. The landscape is evolving with major players still driving multi-billion-dollar deals in incretins and several big names focusing on quality rather than purely quantity of weight loss. Incretin-based therapies accounted for 13 deals worth $25.6 billion in 2024. Proven efficacy means that these therapies continue to attract significant investment.

However, non-incretin targets such as CB1, MC4R, and myostatin/activin are gaining attention. These targets offer the potential to reduce side effects, improve tolerability, preserve lean mass and maintain long-term weight control, addressing some of the limitations of current GLP-1 therapies. Amylin analogues are also resurging, with Roche and Zealand’s $5.25 billion Petrelintide co-commercialization deal serving as a notable example.

This evolving target landscape reflects a strategic shift toward more holistic and differentiated treatment approaches. Companies are looking beyond traditional pathways to develop therapies that offer improved safety, efficacy, and patient outcomes.

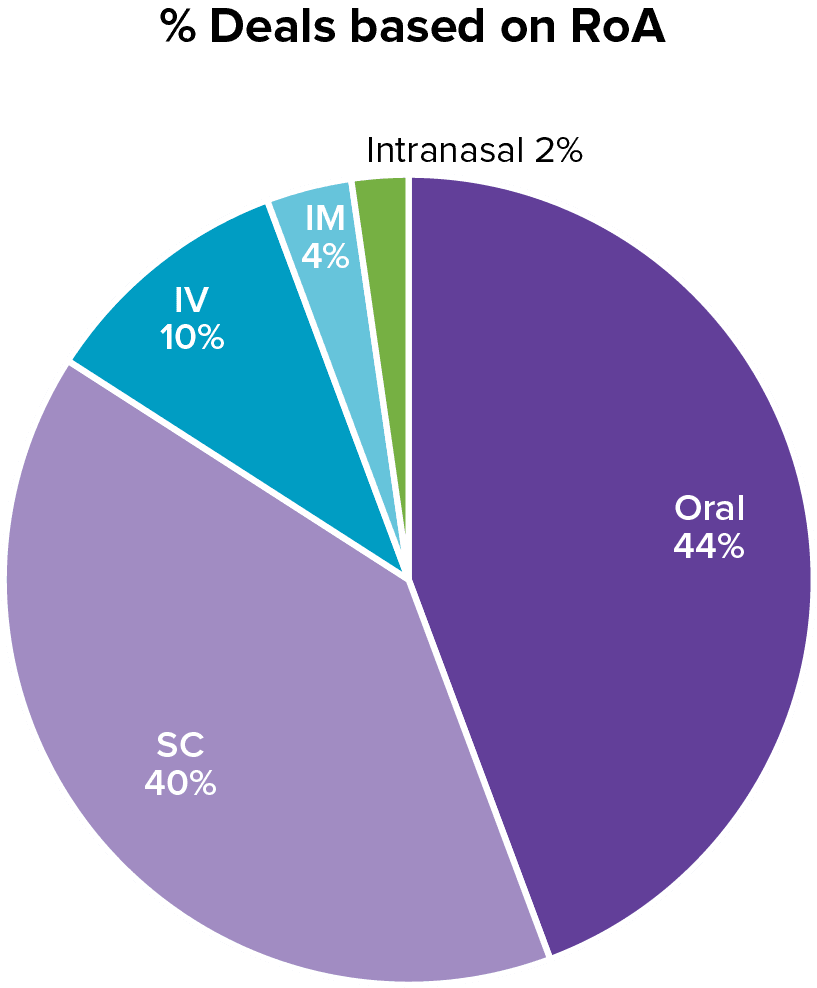

Route of administration (RoA) is becoming a key differentiator. While oral drugs led in deal volume, accounting for 45% of transactions over the past five years, subcutaneous assets dominated in value. Subcutaneous deals reached $30.5 billion in 2024–2025, driven by blockbuster transactions.

Oral therapies are attractive for their convenience, cost-effectiveness, and improved patient compliance. They also alleviate cold-chain requirements and reduce manufacturing costs. Daily dosing allows for more flexible titration compared to weekly injectables, potentially leading to better outcomes with fewer tolerability issues.

Key oral deals include Sciwind & Verdiva’s $2.47 billion licensing agreement and MSD & Hansoh’s $2 billion oral GLP-1 deal. These transactions underscore the growing demand for patient-friendly alternatives to injectable therapies.

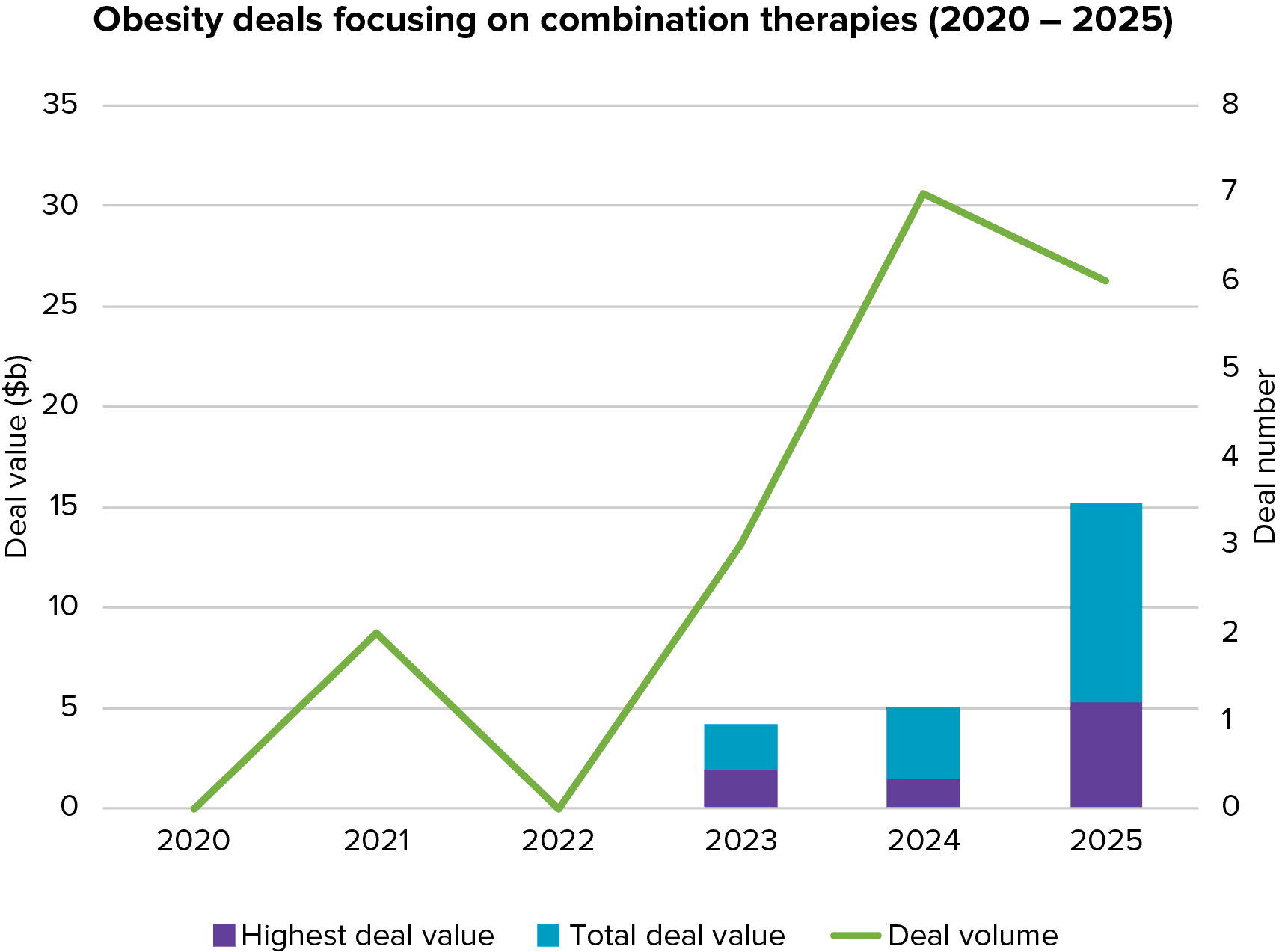

Combination therapies are reshaping the obesity treatment landscape. In 2024–2025, 13 major deals worth $13.6 billion focused on combining GLP-1s with agents targeting amylin, myostatin, or calcitonin pathways. These combinations aim to enhance efficacy, reduce gastrointestinal side effects, and preserve muscle mass.

Examples include Regeneron & Hansoh’s $2 billion GLP-1/GIP + anti-myostatin combo, Roche & Zealand’s $5.25 billion Petrelintide + CT-388 co-formulation, and AbbVie & Gubra’s $2.23 billion long-acting amylin licensing deal. These deals reflect a strategic pivot from monotherapies to more comprehensive treatment regimens.

Daily dosing allows for more flexible titration.

Combination therapies are reshaping the obesity treatment landscape.