The obesity market remains an attractive proposition

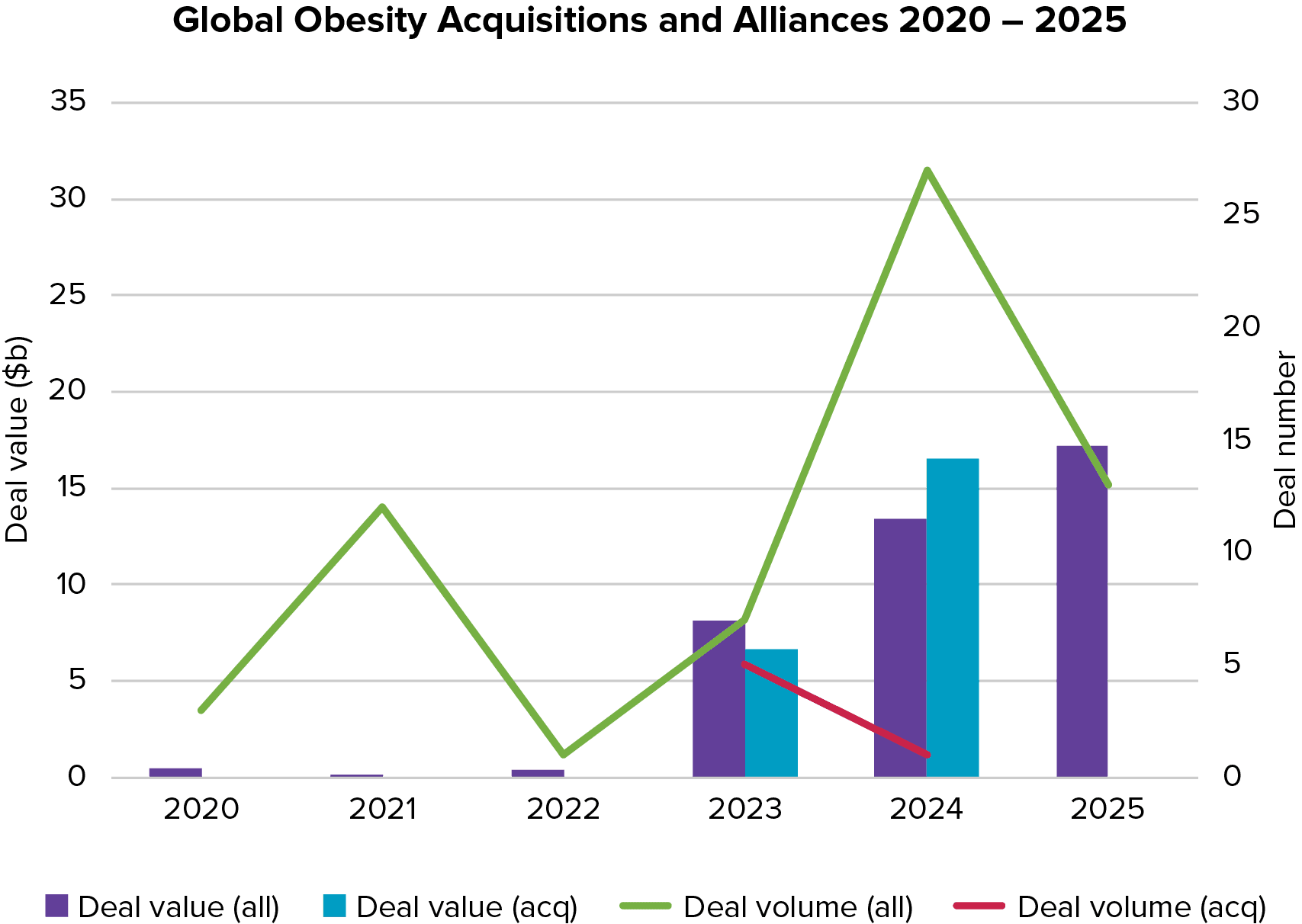

In 2024, biopharma companies established alliances and acquisitions totaling $30bn across 28 deals – an upward trajectory that is expected to continue.

Big pharma such as Lilly, Novo Nordisk, Roche, AstraZeneca, and Pfizer, are typically pursuing a franchise strategy via internal development or in-licensing of obesity assets with diverse mechanisms of action, modalities and routes of administration, to position themselves to meet patient needs across the entire patient journey. These companies are also working to mitigate safety and tolerability issues with GLP1s via co-administration, co-formulations and sequential dosing.

The need to manage the lifecycle of obesity portfolios will see a further drive in deal-making, and while partnerships remain a key entry point, acquisitions are increasingly being used to solidify competitive advantage and ensure supply chain resilience in a rapidly evolving market.