Foreword

The global market for obesity therapeutics has undergone a seismic shift, catalyzed by the rise of GLP-1-based therapies which in turn has driven a surge in strategic dealmaking.

Between 2020 and 2025, over $71 billion was committed across 128 transactions.

Evaluate’s latest analysis reveals that between 2020 and 2025, over $71 billion was committed across 128 transactions, with 2024 alone accounting for $30 billion in alliances and acquisitions. This unprecedented activity reflects a growing recognition of obesity as one of the most pressing global health challenges.

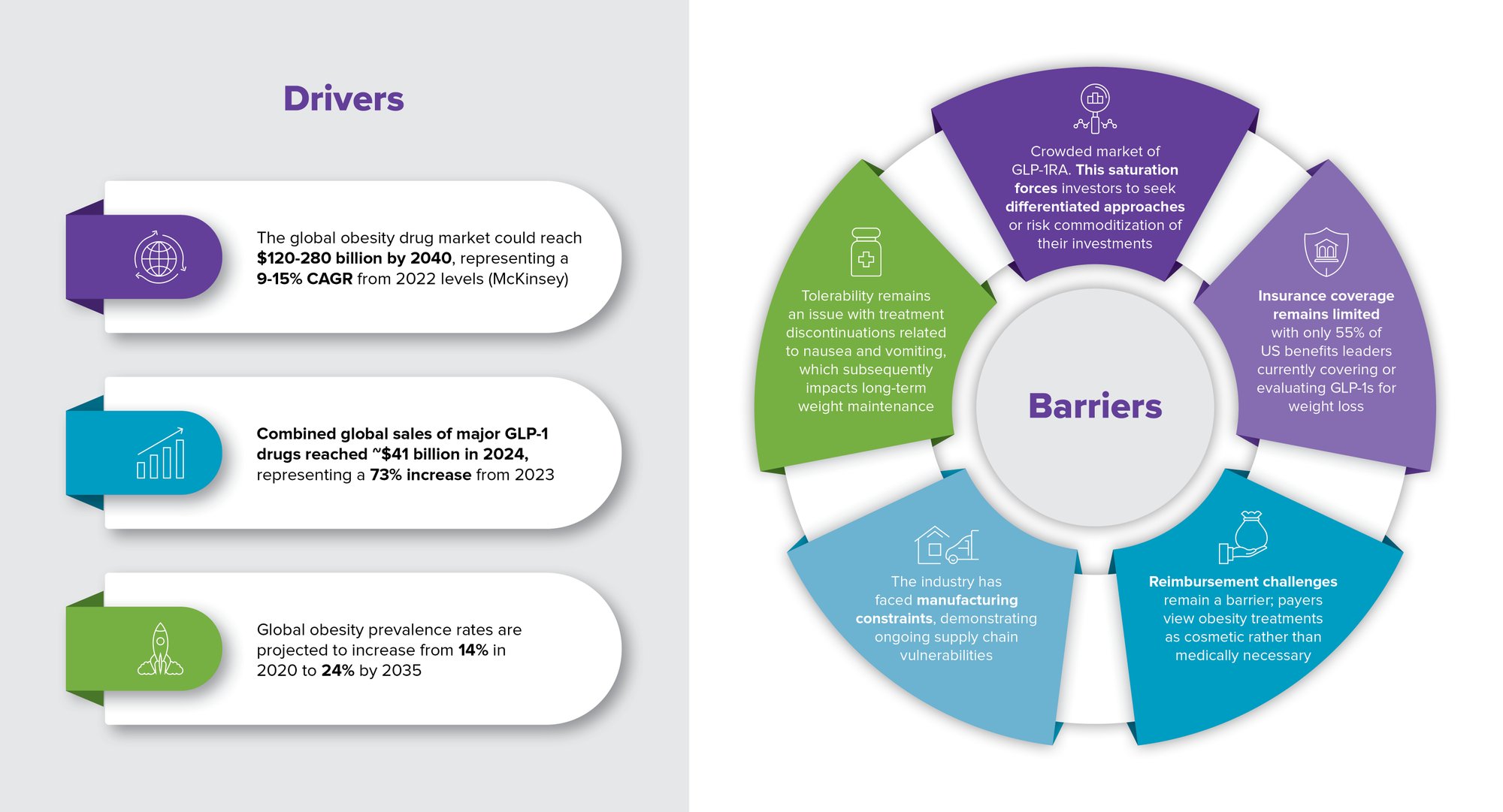

The commercial potential is staggering. According to McKinsey, the obesity drug market could reach between $120 billion and $280 billion by 2040, representing a compound annual growth rate of 9-15% from 2022 levels. This growth is underpinned by rising global prevalence and the success of GLP-1 receptor agonists, which generated $41.4 billion in global sales in 2024 alone, a 73% increase from the previous year. According to the recent Evaluate World Preview report, by 2030, GLP-1 agonists and related combinations will comprise close to 9% of all prescription drug sales.

Yet, the market is not without its challenges. Despite the clinical efficacy of GLP-1s, issues such as limited insurance coverage, reimbursement hurdles, manufacturing constraints and safety/tolerability persist. And the market is becoming increasingly crowded, prompting investors and pharma companies to seek differentiated approaches to avoid commoditization.