The Deal Landscape

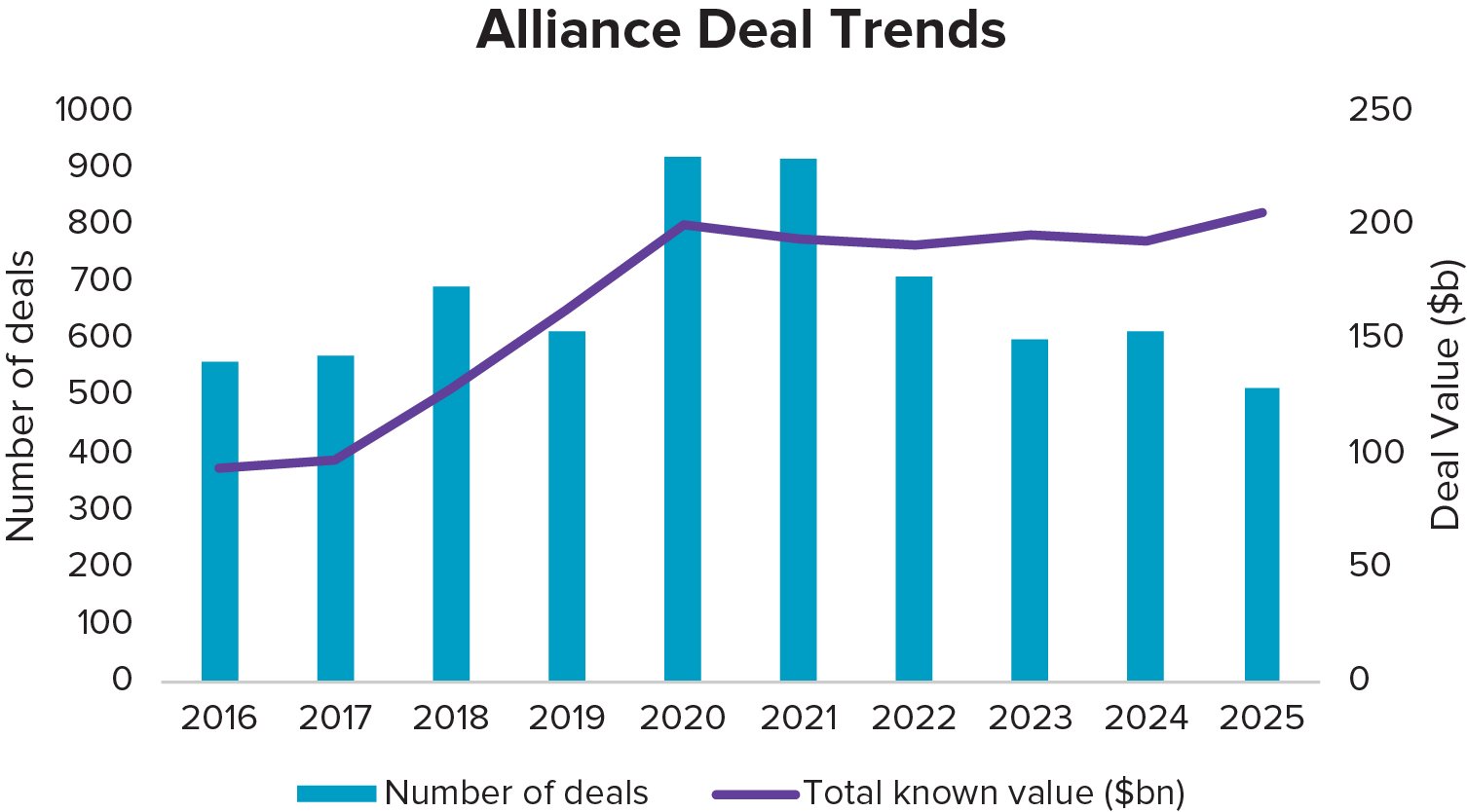

The biopharma deal landscape has evolved rapidly. While alliance and M&A trends have historically followed similar paths, 2025 stands out for a shift toward fewer but higher-value licensing deals. Companies are increasingly selective, focusing on assets with the greatest commercial potential and lowest risk profile.Recent M&A activity has been extraordinary (compared with recent quarters) , with several multi-billion-dollar deals completed through Q3 2025. Notable examples include Novo Nordisk’s $4.7bn acquisition of Akero, Pfizer’s $4.9bn purchase of Metsera, and Merck & Co.’s $10bn bid for Verona. These deals underscore the industry’s willingness to invest heavily in assets that promise to reshape therapeutic landscapes, especially in highly lucrative and growing therapeutic areas like metabolic disease and respiratory care.Regulatory uncertainty, especially in the US, has been a headwind. Now, the policy environment is clearing, improving the outlook for business development. Deal volume peaked in 2021 during the post-Covid rush and has since declined, but total deal value remains robust, indicating a focus on quality over quantity.

2025 stands out for a shift toward fewer but higher-value licensing deals.

For this report we have used several Evaluate data sets, including Evaluate Pharma, and Omnium to identify mechanisms and technologies driving innovation. The analysis applies a weighted ranking approach, considering number of deals, total and average deal value, worldwide peak sales, and current net present value (NPV).Trends are analyzed across three periods: 2015–2018, 2019–2021, and 2022–2025. This view identifies mechanisms and technologies rising or falling in prominence, providing a dynamic picture of industry priorities.The result is a prioritized list of mechanisms and technologies, agnostic to therapeutic area, reflecting where the industry is placing its bets for future success.

While the bulk of our analysis has taken an therapy area agnostic approach, it’s useful to understand the context of the dealmaking landscape.

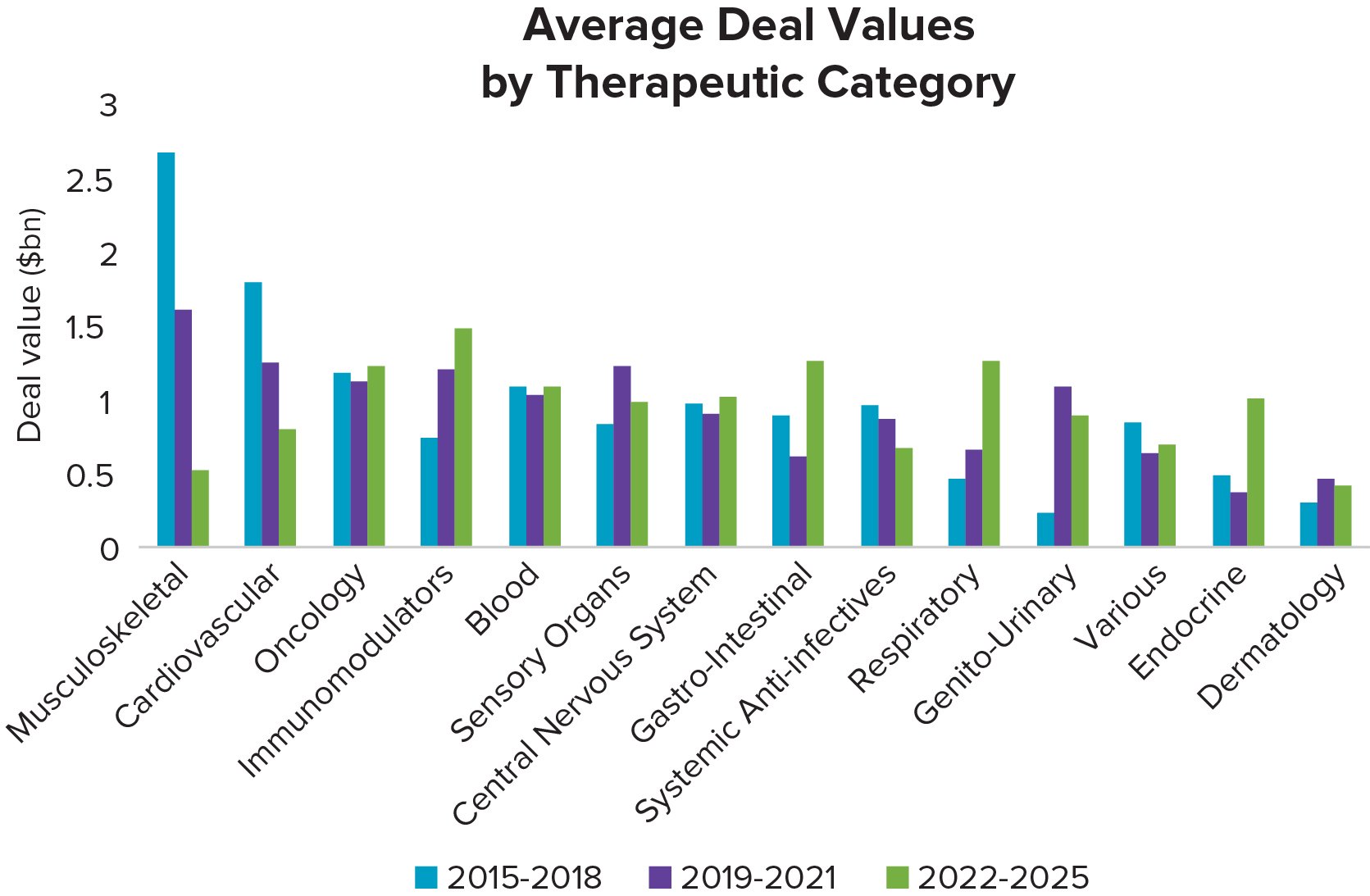

Oncology deal values are consistently driving the deal landscape throughout all the years of this analysis (total of $392bn between 2022-2025) however in the same time period 2022-2025 immunomodulators took the number one spot in terms of average deal values of $1.47bn. This implies that even though fewer deals are done around immunomodulators, they are higher value deals.

Based on total deal values, CNS follows as close second and systemic anti-infectives have seen their lowest value deal especially driven by the Covid-19 pandemic. Cardiovascular diseases have seen an increase in average deal values and moving away from generic small molecules to potentially new technologies.

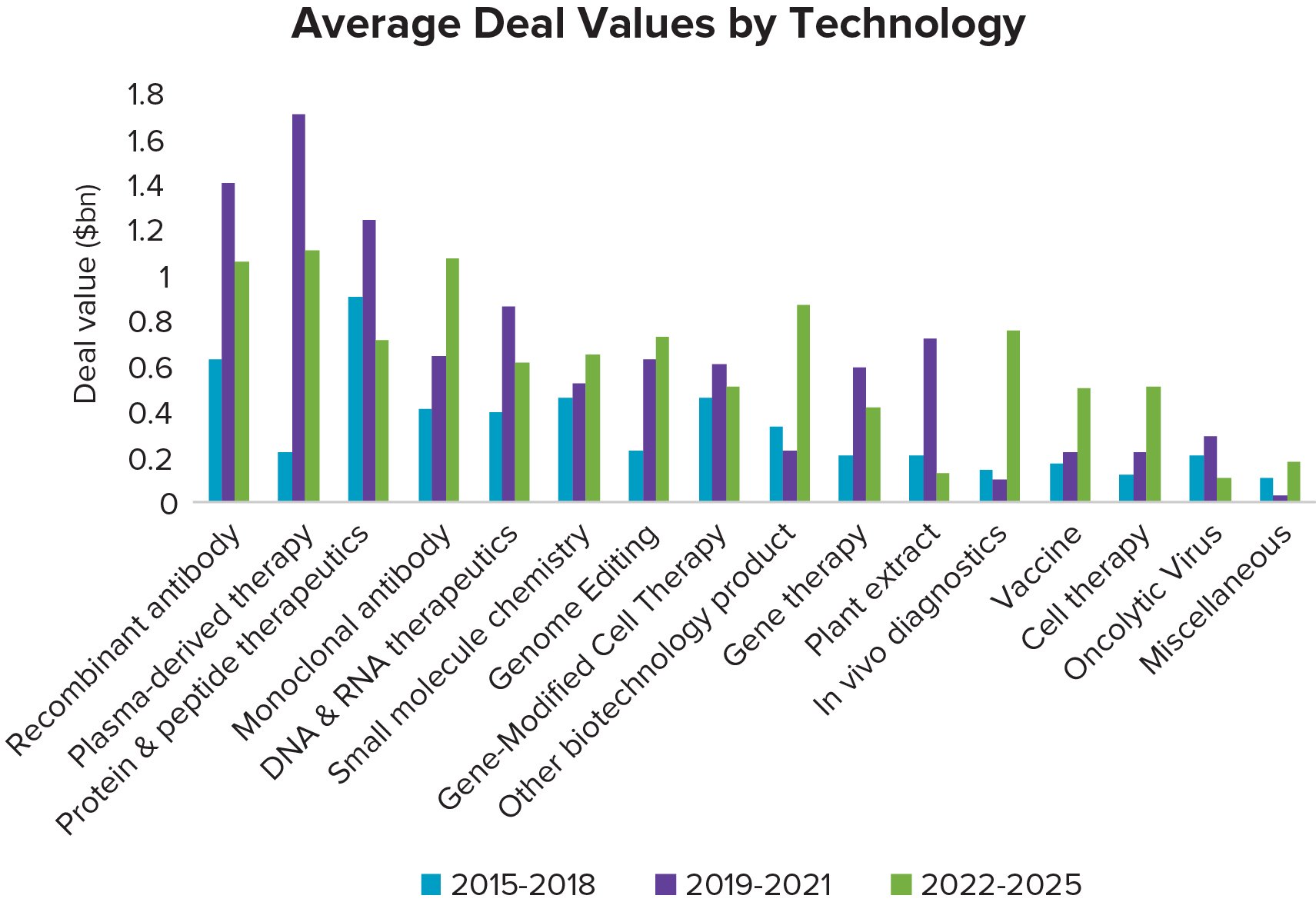

Looking at the top technologies, it’s clear that biologics continue to dominate deal activity with recombinant antibody and protein & peptide therapeutics featuring near the top of the list. This reflects the industry's shift toward complex, targeted therapies with better efficacy and safety profiles. DNA & RNA therapeutics are also rising, initially driven by the success of mRNA vaccines during Covid, but are expanding applications in rare diseases and oncology.

This reflects the industry's shift toward complex, targeted therapies with better efficacy and safety profiles.